Annual Reports

Dingdong (Cayman) Limited's annual reports contain management's most considered account of the business. These are the sections, passages and visual pages worth opening in the originals preserved in Sources.

Dingdong (Cayman) Limited — FY2025 Annual Report (Form 20-F) — FY2025

The latest 20-F, and a pivotal one: it discloses the February 2026 agreement to sell substantially all China operations to Meituan. · Open the full document →

Item 3. Key Information — D. Risk Factors — p. 13 · Read the full section →

The two risks that are specific to this business right now: a mid-flight divestiture to Meituan, and the food-safety exposure inherent to fresh grocery.

The Meituan sale risk: deconsolidation, loss of users/key employees, and a five-year non-compete on To-C grocery in Greater China.

The sale of Dingdong Fresh BVI to the Buyer may adversely affect our business, financial condition or results of operations, our relationships with our current and potential users and employees of Dingdong Fresh BVI, and could result in the loss of our users and key employees. The deconsolidation of Dingdong Fresh BVI after the closing of the Transaction may adversely affect our results of operations and future development strategy. Together with the transaction, we and Mr. Changlin Liang have entered into a five-year non-competition and non-solicitation covenant with the Buyer, which may pose potential restrictions to our To-C fresh grocery e-commerce business within the Greater China region and may adversely affect our relationship wit existing partners and may have an adverse effect on our future growth prospects. After the closing and certain customary matters to be completed, there ca be no assurance that we may achieve anticipated strategic benefits.

p. 16 · Read in context →

Food-safety exposure: a 7+1 quality-control process, but pesticide and heavy-metal residues have slipped through before.

Although we have developed end-to-end quality control procedures through our 7+1 Quality Control Procedure across the entire procurement and fulfillment process, we cannot assure you that we can always identify every quality control issue due to potential flaws, loopholes and bugs of our procedures and human errors, and our efforts to patch up or update our quality control procedures may suffer from delays or failures due to external factors not entirely under our control. In addition, there are inherent limitations in sampling inspection of non-standard products such as fresh produce, seafood meats, which may not identify all the defects and flaws. Our business growth and development, which result in increased cooperation with an increasing number of suppliers and business partners, evolving and increasingly complex supply chain, and continued digitalization of the fulfillment process all possess the potential to exacerbate the pressure on our quality control procedures, which are in turn required to be perfected in a timely manner. We have detected and remedied several cases of sub-par products being sold on Dingdong Fresh, e.g. excessive pesticide or heavy metal residues. Despite our rectification efforts, we are unable to entirely rule out the possibility that similar incidents will take place again in the future.

p. 19 · Read in context →

Item 4. Information on the Company — p. 54 · Read the full section →

Management's own description of the model — a self-operated frontline fulfillment grid and direct-sourced private label — and where the Meituan deal terms are set out.

The deal terms: US$717m cash plus up to ~US$997m total from Meituan's buyer; international business retained; pending SAMR clearance.

On February 5, 2026, we entered into a definitive Share Purchase Agreement (the “Share Purchase Agreement”) with Two Hearts Investments Limited (the “Buyer”), a wholly-owned subsidiary of Meituan (HKEX: 3690). Pursuant to the Share Purchase Agreement, we have agreed to sell to the Buyer all issued and outstanding shares of Dingdong Fresh BVI, which holds through a series of wholly-owned and majority equity interest subsidiaries substantially all of our operations in China (the “Transaction”). The Buyer will pay cash consideration of US$717 million in the Transaction. In addition, we will have the right to receive prior to August 31, 2026 total cash not exceeding US$280 million from Dingdong Fresh BVI and its subsidiaries (provided that the total net cash of Dingdong Fresh BVI and its subsidiaries on a consolidated basis as of December 31, 2025 minus such amounts received by us shall not be less than US$150 million). As such, we expect that it will receive up to US$997 million in cash proceeds from the Transaction. Thi amount is subject to certain adjustments, including those based on certain net cash, net working capital and other financial line item thresholds of Dingdong Fresh BVI and its subsidiaries as of certain agreed upon dates. In the event that the net cash of Dingdong Fresh BVI and its subsidiaries on a consolidated basis as of December 31, 2025 minus the amounts received by us as described above is less than US$150 million, the Buyer has the right to adjust the purchase price cash consideration at closing for any such shortfalls. Our international business is not part of the Transaction and will be retained by us following any necessary reorganizational processes to be completed prior to the closing of the Transaction. As of the date of this annual report, th Transaction has not been completed, and is subject to the satisfaction or waiver of various customary conditions set forth in the Share Purchase Agreement, including the receipt of anti-monopoly clearance from the SAMR.

p. 54 · Read in context →

Scale and the 2021 pivot to “efficiency first” — GMV of RMB26.4bn and thirteen straight non-GAAP-profitable quarters.

As a result, we have achieved significant scale in our business, and accumulated a massive and highly active user base. Our GMV increased from RMB21,969.3 million in 2023 to RMB25,557.4 million in 2024, and further increased to RMB26,436.2 million (US$3,780.3 million) in 2025. Starting from the third quarter of 2021, we strategically shifted our focus to “efficiency first with due consideration of scale”, aiming to achieve profitability to maximize our investors’ interests in us. Ever since our strategic shift, we have been focusing on further strengthening our product competitiveness while optimizing our fulfillment network, so as to increase user stickiness and secure their loyalty with us. Guided by the strategy, we have achieved non-GAAP profitability for thirteen consecutive quarters and GAAP profitability for eight consecutive quarters.

p. 55 · Read in context →

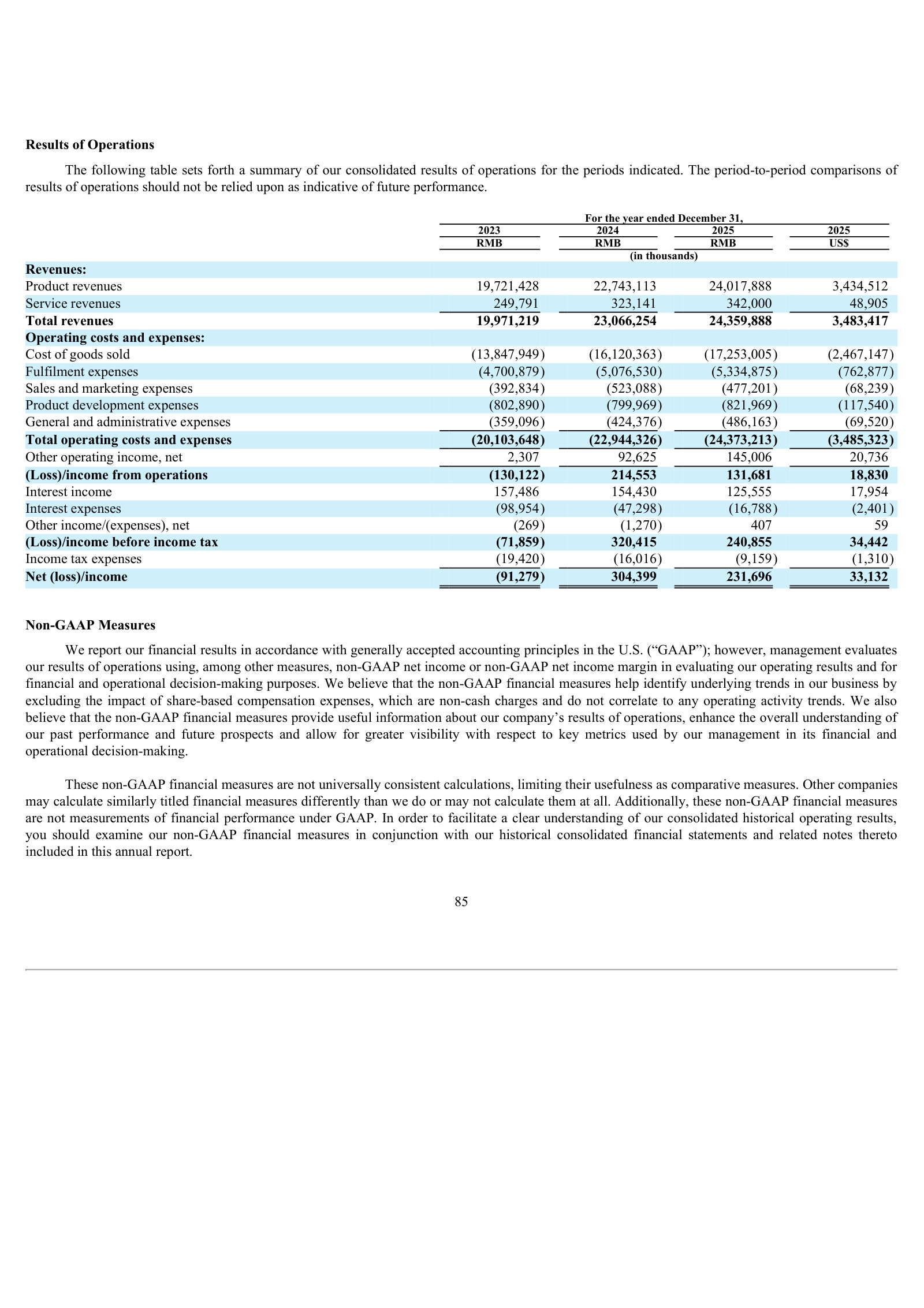

Item 5. Operating and Financial Review and Prospects — p. 85 · Read the full section →

Where management explains a thin-margin scale business: revenue growth drivers and the cost ratios that decide whether it makes money.

What drove FY2025 revenue (+5.6%): more orders, higher order frequency, new East-China stations, and growing overseas B2B.

Our revenues increased from RMB23,066.3 million in 2024 to RMB24,359.9 million (US$3,483.4 million) in 2025.

Product revenues. Product revenues increased from RMB22,743.1 million in 2024 to RMB24,017.9 million (US$3,434.5 million) in 2025, mainl due to the rise of number of orders resulting from rise in the average monthly number of transacting users and higher monthly order frequency, and new opened frontline fulfillment stations with density and market penetration improved in East China. Additionally, our B2B revenue achieved year-over-year growth, with the revenue contribution from overseas B2B operations continuing to increase and posting rapid sequentially

p. 91 · Read in context →

Item 5. Critical Accounting Policies, Judgments and Estimates — p. 94 · Read the full section →

Gross-basis revenue recognition is why RMB24bn flows through the P&L — it defines Dingdong as a first-party retailer that owns inventory, not a marketplace.

Revenue booked gross because Dingdong is the principal — it fulfills the goods, takes inventory risk, and sets prices.

We recognize product sales made through Dingdong Fresh APP, mini-programs and third-party platforms on a gross basis because we are acting as the principal in these transactions as we (i) are responsible for fulfilling the promise to provide the specified goods, (ii) take on inventory risks and (iii) have discretion in establishing price.

p. 95 · Read in context →

More annual reports

Dingdong (Cayman) Limited — FY2024 Annual Report (Form 20-F) — FY2024 · 201 pages · The pre-divestiture baseline: first full year of GAAP profitability with the China grocery network still fully intact. · Open →

Dingdong (Cayman) Limited — FY2023 Annual Report (Form 20-F) — FY2023 · 192 pages · Shows the “efficiency first” retrenchment year — network pruning and cost discipline on the road to profitability. · Open →

Dingdong (Cayman) Limited — FY2022 Annual Report (Form 20-F) — FY2022 · 178 pages · The strategic-shift year: management reframes from scale-at-all-costs growth to profitability after the Q3 2021 pivot. · Open →

Dingdong (Cayman) Limited — FY2021 Annual Report (Form 20-F) — FY2021 · 352 pages · The first 20-F after the June 2021 NYSE IPO — the original scale-first growth story before the profitability pivot took hold. · Open →