Full Report

The numbers behind Dingdong (Cayman) Limited: as-reported financial statements and company metrics for FY2021–FY2025, traced to the source filings. Every linked figure opens the exact page of the filing it was printed on, with the statement row highlighted. Amounts in RMB millions (¥) unless noted.

Reading notes: Reporting currency is RMB (Renminbi); the company files under U.S. GAAP as a foreign private issuer (Form 20-F). All figures are in RMB millions as filed (the filings print thousands of RMB; values here are divided by 1,000 and rounded). The filings also show a US$ convenience translation, which is not used here. Shares trade on the NYSE as ADSs (2 ADS = 3 ordinary shares) in USD. Each fiscal year is cited to the most recent 20-F that presents it on a consistent (post-reclassification) basis: FY2023–FY2025 income cash-flow columns from the FY2025 20-F; FY2022 from the FY2024 20-F; FY2021 from the FY2023 20-F. Balance sheets: FY2024–FY2025 from the FY2025 20-F, FY2022–FY2023 from the FY2023 20-F, FY2021 from the FY2022 20-F. Per-ordinary-share amounts are as printed. FY2021 basic/diluted loss per share of RMB(34.50) reflects the low pre-IPO weighted-average share count (194.7mn) plus preferred-share accretion in the IPO year and is not comparable with later years. Long-Term Record: FY2019–FY2020 total revenue and net loss are taken from the FY2021 20-F (Form 20-F, three-year comparative columns). FY2019 diluted EPS and FY2019 operating cash flow are omitted (pre-IPO share structure / not extracted). FY2020 operating cash flow is from the FY2022 20-F.

FY2025 at a Glance

Revenue (RMB millions (¥))

Diluted EPS

Source: FY2025 consolidated statements [1] [2] [3]. Click any linked figure to open the filing page with the row highlighted.

Revenue by Type

| Revenue by Type | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Product revenues | 19,897 | 23,939 | 19,721 | 22,743 | 24,018 |

| Service revenues | 224 | 282 | 250 | 323 | 342 |

| Total revenues | 20,121 | 24,221 | 19,971 | 23,066 | 24,360 |

| Total revenues growth, derived | — | +20.4% | -17.5% | +15.5% | +5.6% |

Source: Consolidated Statements of Comprehensive (Loss)/Income — disaggregation of revenue (Note 3) [1] [2] [3]. Click any linked figure to open the filing page with the row highlighted.

Income Statement

Source: Consolidated Statements of Comprehensive (Loss)/Income [1] [2] [3]. Click any linked figure to open the filing page with the row highlighted.

Columns marked E are consensus analyst estimates shown alongside reported results for direct comparison; they are not company guidance.

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-19. Estimate figures link to the consensus source, not to filing pages.

Balance Sheet

| Balance Sheet | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Cash and cash equivalents | 663 | 1,856 | 1,209 | 887 | 1,107 |

| Short-term investments | 4,568 | 4,637 | 4,100 | 3,562 | 2,870 |

| Inventories, net | 537 | 605 | 472 | 554 | 570 |

| Total current assets | 6,516 | 7,496 | 6,151 | 5,365 | 5,040 |

| Property and equipment, net | 472 | 315 | 189 | 176 | 233 |

| Operating lease right-of-use assets | 2,246 | 1,425 | 1,262 | 1,465 | 1,580 |

| Total assets | 9,420 | 9,382 | 7,699 | 7,118 | 7,016 |

| Accounts payable | 2,059 | 1,887 | 1,422 | 1,660 | 1,920 |

| Short-term borrowings | 3,121 | 4,238 | 3,300 | 1,606 | 872 |

| Total current liabilities | 7,349 | 8,211 | 6,506 | 5,270 | 4,795 |

| Total liabilities | 8,662 | 8,964 | 7,200 | 6,194 | 5,840 |

| Total shareholders' equity | 728 | 310 | 383 | 799 | 1,041 |

Source: Consolidated Balance Sheets (as of December 31) [4] [5] [6] [7]. Click any linked figure to open the filing page with the row highlighted.

Cash Flow

| Cash Flow | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Net cash (used in)/generated from operating activities | (5,667) | 87 | (235) | 929 | 536 |

| Purchases of property and equipment | (452) | (127) | (83) | (98) | (178) |

| Net cash (used in)/generated from investing activities | (4,065) | (47) | 519 | 476 | 430 |

| Repurchase of ordinary shares | (3) | (18) | 0 | (31) | (9) |

| Net cash generated from/(used in) financing activities | 9,043 | 1,112 | (934) | (1,724) | (743) |

| Net increase/(decrease) in cash and cash equivalents and restricted cash | (780) | 1,189 | (649) | (319) | 217 |

| Free cash flow, derived | (6,119) | (40) | (318) | 831 | 358 |

Source: Consolidated Statements of Cash Flows [8] [9] [10] [11]. Click any linked figure to open the filing page with the row highlighted.

Marketplace Scale Fulfillment Network

| Marketplace Scale Fulfillment Network | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| GMV (gross merchandise value) | 22,704 | 26,248 | 21,969 | 25,557 | 26,436 |

| Average order value (RMB per order) | 58.7 | 74.5 | 72.1 | 71.4 | 70.1 |

| Frontline fulfillment stations | 1,300 | 1,100 | 1,000 | 1,000 | 1,100 |

| Cities covered | 35 | 30 | 25 | 25 | 28 |

| Regional processing centers | 60 | 60 | 45 | 40 | 40 |

Source: company filings [12] [13] [14] [15]. Click any linked figure to open the filing page with the row highlighted.

Private-Label Program

| Private-Label Program | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Private-label share of total GMV | — | 16.0% | 20.0% | 20.0% | 20.0% |

| Private-label SKUs | — | 2,200 | 3,000 | 4,000 | 5,000 |

| Private-label brands launched (cumulative) | — | 20 | 30 | 30 | 23 |

Source: company filings [16] [17] [18] [19]. Click any linked figure to open the filing page with the row highlighted.

Profitability Quality of Earnings

| Profitability Quality of Earnings | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Non-GAAP net (loss)/income | (6,114) | (571) | 45 | 423 | 310 |

| Non-GAAP net (loss)/income margin | (30.4%) | (2.4%) | 0.2% | 1.8% | 1.3% |

| Government subsidies recognized (operating + non-operating) | 16.8 | 15.0 | 18.1 | 61.0 | 87.4 |

Source: company filings [20] [13] [21] [22]. Click any linked figure to open the filing page with the row highlighted.

Long-Term Record

| Fiscal year | Total revenues | Net (loss)/income | Diluted (loss)/earnings per ordinary share | Net cash from operating activities |

|---|---|---|---|---|

| FY2019 | 3,880 | (1,873) | — | — |

| FY2020 | 11,336 | (3,177) | — | (2,056) |

| FY2021 | 20,121 | (6,429) | (34.50) | (5,667) |

| FY2022 | 24,221 | (807) | (2.51) | 87 |

| FY2023 | 19,971 | (91) | (0.31) | (235) |

| FY2024 | 23,066 | 304 | 0.90 | 929 |

| FY2025 | 24,360 | 232 | 0.66 | 536 |

Source: consolidated statements across filings; older years from the standardized feed [9] [1] [11] [2]. Click any linked figure to open the filing page with the row highlighted.

Operating KPIs

| KPI | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| GMV (gross merchandise value) | 22,704.1 | 26,247.9 | 21,969.3 | 25,557.4 | 26,436.2 |

Source: company-reported operating metrics [13] [23]. Click any linked figure to open the filing page with the row highlighted.

Analyst Consensus

Current price

Mean target

Median target

High target

Low target

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-19. Estimate figures link to the consensus source, not to filing pages.

Traceability

288 of 289 figures on this page (100%) link to the filing page where they are printed — click a linked figure to open the source PDF at that page with the row highlighted. Unlinked figures come from standardized data feeds or pre-filing years.

Reporting currency is RMB (Renminbi); the company files under U.S. GAAP as a foreign private issuer (Form 20-F). All figures are in RMB millions as filed (the filings print thousands of RMB; values here are divided by 1,000 and rounded). The filings also show a US$ convenience translation, which is not used here. Shares trade on the NYSE as ADSs (2 ADS = 3 ordinary shares) in USD.

Each fiscal year is cited to the most recent 20-F that presents it on a consistent (post-reclassification) basis: FY2023–FY2025 income cash-flow columns from the FY2025 20-F; FY2022 from the FY2024 20-F; FY2021 from the FY2023 20-F. Balance sheets: FY2024–FY2025 from the FY2025 20-F, FY2022–FY2023 from the FY2023 20-F, FY2021 from the FY2022 20-F.

Per-ordinary-share amounts are as printed. FY2021 basic/diluted loss per share of RMB(34.50) reflects the low pre-IPO weighted-average share count (194.7mn) plus preferred-share accretion in the IPO year and is not comparable with later years.

Long-Term Record: FY2019–FY2020 total revenue and net loss are taken from the FY2021 20-F (Form 20-F, three-year comparative columns). FY2019 diluted EPS and FY2019 operating cash flow are omitted (pre-IPO share structure / not extracted). FY2020 operating cash flow is from the FY2022 20-F.

Quarterly block covers the whole group on a consistent basis (Q1 FY2024–Q4 FY2025), income statement only; each quarter is a single three-month period taken from that quarter's earnings release (unaudited). NOTE: beginning Q1 FY2026 the company reclassified its China business as discontinued operations (planned disposal; overseas business = continuing operations), which breaks comparability with these periods, so Q1 FY2026 is deliberately excluded from the quarterly series.

Segment reporting: the CODM manages the business as a single reportable segment; revenue is disaggregated only into Product revenues and Service revenues (the revenue-breakdown table above), so no separate segment-profit statement is presented.

GMV (gross merchandise value) is an operating metric disclosed in Item 5 of each 20-F; it is larger than reported revenue and is shown as a KPI in RMB millions.

3 figure(s) differed between the data feed and the filing; the filing value is shown (see the run's metrics/metrics_tab.json for the audit trail).

Dingdong (Cayman) Limited's management explains the business in its own materials. The slides below do the most of that work, pulled from the documents preserved in Sources. Each source link opens the complete presentation at that slide in a new tab.

2025 Q3 Results — Q3 2025

The latest quarterly deck — current scale, unit economics, cost structure and the One Big/One Small/One World strategy in one place. · Open the full document →

2023 Q3 Results — Q3 2023

Where management explains what Dingdong actually is — a vertically integrated food company, not just a delivery app. The clearest statement of the model. · Open the full document →

2023 Q2 Results — Q2 2023

Two operating slides the later decks stopped showing: the economics of membership and how the supply chain is actually run. · Open the full document →

More from management

2025 Q1 Results — Q1 2025 · 11 pages · The 4G strategy (good users, products, services, mindshare) and ecosystem framing that precedes the current One Big/One Small/One World language. · Open →

2024 Q3 Results — Q3 2024 · 10 pages · The record quarter — GMV +28% YoY and non-GAAP profit up nearly 10x — the inflection to which recent results are compared. · Open →

2024 Q2 Results — Q2 2024 · 11 pages · Management's articulation of future growth drivers: deepening Jiangsu/Zhejiang/Shanghai and reusing spare supply-chain capacity. · Open →

2024 Q1 Results — Q1 2024 · 10 pages · A cleaner, later restatement of the supply-chain thesis — end-to-end efficiency as the fundamental principle for the fresh-grocery business. · Open →

2023 Q4 and Full-Year Results — Q4/FY2023 · 10 pages · The full-year 2023 wrap-up — first year of sustained non-GAAP profitability and the private-label penetration picture. · Open →

Dingdong (Cayman) Limited's management answers for the business every quarter. These are the exchanges that explain it best — verbatim, from the call transcripts preserved in Sources. Each link opens the full transcript at that page in a new tab.

Q3 FY2025 Earnings Call — Q3 FY2025

The most recent call: how Dingdong plans to grow through an intensifying price war — the "One Big, One Small, One World" framework and the top-selling-product model, in management's own words. · Open the full transcript →

How the "Good Products" system compounds retention, order frequency and GMV.

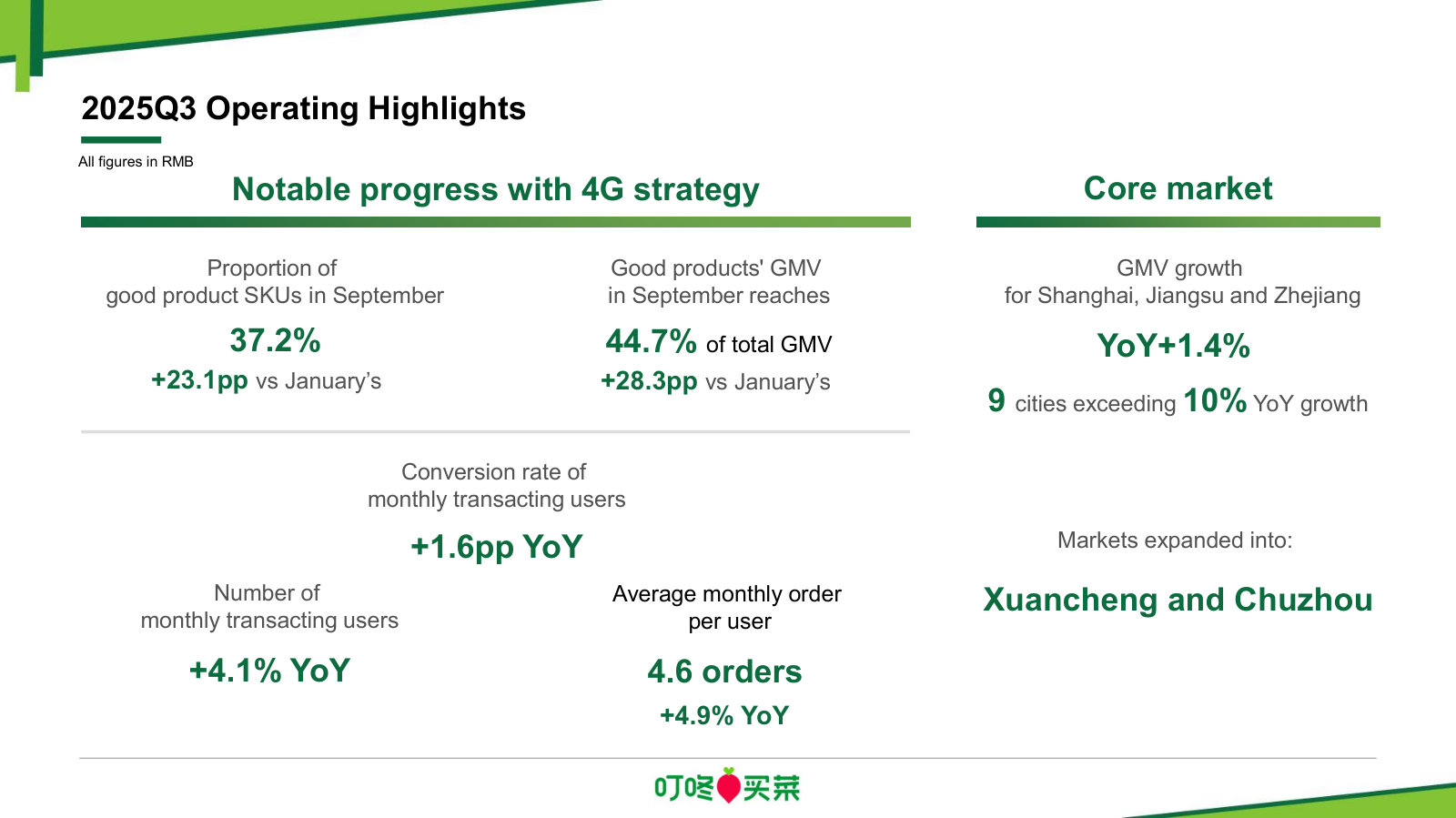

Changlin Liang (Founder & CEO): This year, the company has made notable progress with its "Good Products" system. A series of good products has effectively enhanced user retention and repurchase rates, while also significantly supporting overall GMV growth. For instance, in September, SKUs classified as "Good Products" comprised 37.2%, generating 44.7% of total GMV—a rapid jump from January, when the 4G strategy was launched, and the share of Good Products SKUs was 14.1% and their GMV contribution was 16.4%. The growing number of these "Good Products" has attracted more users to place orders on Dingdong. In Q3, the monthly order conversion rate increased by 1.6 percentage points year-over-year, and the number of monthly ordering users grew by 4.1%. Additionally, "Good Products" have further strengthened user mindshare. The average monthly order frequency reached a record 4.6 times in Q3—up 4.9% year-over-year with member placing an average of 7.7 orders per month, a 1.3% year-on-year increase.

p. 2 · Read in context →

Where the money comes from: flat GMV, B2B up 67%, and margin managed by design.

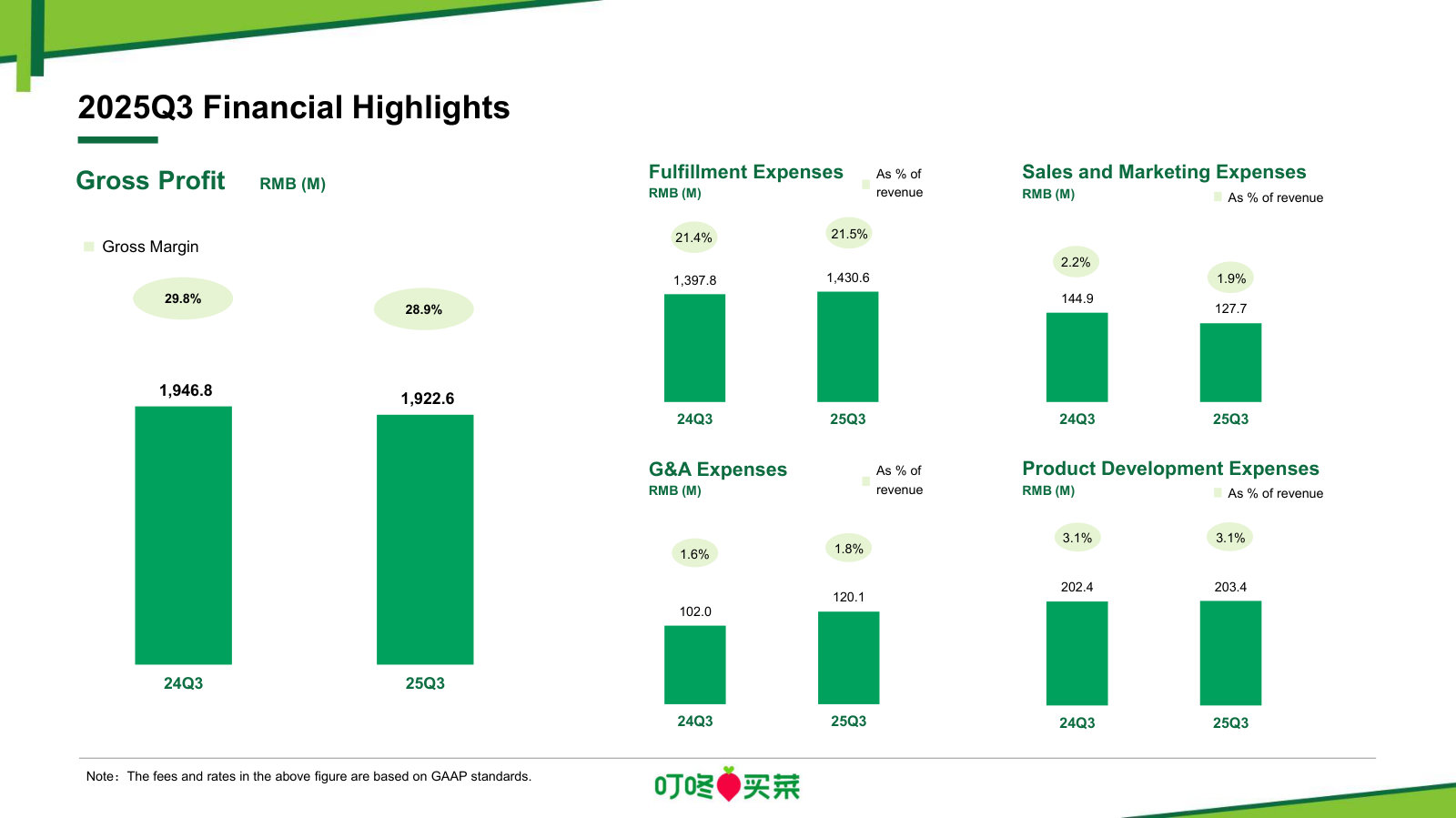

Song Wang (CFO): Revenue for Q3 reached RMB 6.66 billion, marking a 1.9% year-on-year increase. GMV was RMB 7.27 billion, up 0.1% compared to the previous year. The scale growth mainly stemmed from a general rise in order volume, which increased by 2.2% year-on-year in Q3. This quarter, our B2B business continued to grow steadily, with revenue expanding by 67.4% year-on-year, and its revenue share rose by 1.9 percentage points year-on-year. […] Gross profit margin was 28.9%, down 0.9 percentage points year-on-year. The decline in gross profit narrowed on a quarter-on-quarter basis. During the quarter, the company maintained its focus on its "good products" strategy by refining its product lineup, emphasizing flagship items, and increasing the supply of high-quality goods. It continued to enhance its supply chain system by prioritizing high-quality products that meet market demand, while systematically phasing out slow-moving items with low user preference. This "high-quality in, low-quality out" approach enabled the company to focus on core categories, thereby enhancing overall product competitiveness.

p. 4 · Read in context →

Q2 FY2025 Earnings Call — Q2 FY2025

The fullest account of the 4G strategy reset — the org redesign, the full-chain AI build-out, and a six-point contrast with the platform rivals. · Open the full transcript →

The operating model in one frame: 85% direct sourcing, omnichannel demand, widening geography.

Changlin Liang (Founder & CEO): First, we strengthened our presence in the supply chain by sourcing over 85% of our fresh produce directly from the origin, including Dingdong Agriculture, Guyu Factory, ten product development divisions, Dingdong Xiaoman origin procurement, and direct sourcing from Australia. This ensured ample product availability – in other words, always stock on hand. Second, on the demand side, we expanded omnichannel sales. Besides our popular Dingdong app, we also served domestic and international KA channels and B2B clients, such as merchants, hotels, travel agencies, restaurants, canteens, and factories. Omnichannel sales boosted sales efficiency and fully showcased the value of our supply chain, leading to "sales success." Lastly, we continuously expanded our operational regions, starting from East China to nationwide coverage, and then gradually entering Southeast Asia, the Middle East, and Central Asia. Looking ahead, we plan to expand into Europe, America, and Africa. These simultaneous efforts across supply chains, channels, and regions formed an interconnected system—"point, line, plane, and solid"—which broke growth barriers and enhanced our core system capabilities and competitiveness.

p. 2 · Read in context →

The full-chain AI strategy — from LLM procurement agents to automated sugar-content testing.

Changlin Liang (Founder & CEO): Dingdong was an early AI adopter and among the first in the industry to extensively embed AI into its business. It now implements a comprehensive full-chain AI strategy across all core business segments. […] Supply Chain Intelligence: We use multimodal technology for smart management and optimization throughout the supply chain, enhancing the accuracy and consistency of mapping between physical and digital environments and ensuring "truth-seeking and traceability" across the entire supply chain. Additionally, a large language model (LLM) agent automates decisions on purchasing, allocation, and promotions, further improving inventory accuracy and system stability. For instance, we developed an automated system for testing fruit sugar content, overhauling the testing process to automate everything from "image recognition to data analysis to system integration," replacing manual data entry. The results are notable: data entry time dropped from 20 seconds to under 3 seconds; accuracy rose significantly to 98.3%, greatly reducing quality disputes caused by human errors; and all test data is automatically synchronized to the system, supporting data analysis and traceability, standardizing data, and boosting management efficiency. This system represents a successful application of intelligent supply chain management in the quality control process.

p. 3 · Read in context →

What the 4G reset actually changed: 10 product divisions, GMV/margin dropped as KPIs, good-user repurchase.

Thomas Chong (Jefferies); Changlin Liang (Founder & CEO): Could you summarize the progress and outcome of the 4G strategy during this period?

Liang Changlin: (Speaking Foreign Language). Thank you for your question. The 4G strategy has been in place for more than six months. During this period, we have refined our production relationships and enhanced productivity, emphasizing "good users, good products, good services, and good mindshare.”

First, we comprehensively restructured our production relationships by dismantling traditional product development centers. We integrated personnel from product development, operations, and quality control to form 10 independent product development divisions, each led by a key executive. This shift enabled the Company to prioritize high-quality products and increase organizational efficiency. Simultaneously, we overhauled resource distribution and performance evaluation methods. During this period, we removed GMV and profit margin as performance metrics, instead emphasizing quality indicators such as the proportion of good products, good users, purchase repeat rate, and negative reviews. […] Our good users show an exceptionally high repurchase rate with at least eight orders monthly per user, compared to the average of 4.4.

p. 5 · Read in context →

Six point-by-point contrasts with the price-war rivals — the clearest statement of the moat.

Yang Bai (CICC); Changlin Liang (Founder & CEO): Since our IPO in 2021, we have been attentive to competition in areas such as community group buying, platform delivery, and frontline fulfillment stations. We have addressed these issues individually in previous quarters. We focus less on competition and more on creating value. Reflecting on this journey, we have stayed consistent and accurate in our understanding and positioning.

First, recent competition within instant retail has garnered widespread attention. The battle for users and traffic is fierce, with many adopting quick, short-term price wars. However, this focus often neglects aspects like supply chains and product development. As we outlined with our strategic approach of "narrower and deep," we differ significantly from typical instant retail companies. […] First, our goal is to develop the supply chain and create an ecosystem, whereas theirs is to compete for more users and traffic.

Second, strategically we emphasize commodity and ecological approaches, unlike their focus on traffic, platform dominance, and market monopolization.

Third, in our relationships with channels we seek win-win cooperation and steady growth, whereas they engage in zero-sum market competition.

Fourth, our interactions with suppliers are collaborative and mutually beneficial, while theirs follow a traditional client-provider model.

Fifth, our business models grow in proportion to our upstream and downstream partners. In contrast, theirs are characterized by a power-law distribution, with a few entities controlling most resources and influence, and becoming oligopolies.

Sixth, we value long-term relationships and patience, unlike their focus on short-term KPIs.

p. 6 · Read in context →

Q2 FY2024 Earnings Call — Q2 FY2024

Return to growth laid bare: the anti-Walmart operating principle, the 0-to-1 / 1-to-10 revenue vision, and hard numbers on new-station unit economics. · Open the full transcript →

Why the Walmart playbook fails in fresh grocery — the first principle Dingdong runs on.

Thomas Chong (Jefferies); Changlin Liang (Founder & CEO): Many in the industry adhere to the traditional retail approach, which is achieving scale by offering low prices and then leveraging that scale to drive down procurement costs and operating expenses. However, we've realized that the first principle of traditional retailing, which has been successful since the Walmart era, is not applicable to the fresh grocery industry.

Instead, the first principle of success is to continuously enhance end-to-end efficiency, to achieve growth at scale, seek profitability and bolster competitiveness. It is crucial that we focus on consistently improving our supply chain capabilities. With these capabilities, we'll be able to serve a larger customer base and meet their evolving needs.

p. 6 · Read in context →

The long-range guidance frame: from 0-to-1 (RMB20bn) to 1-to-10 (RMB100bn) over the next seven years.

Robin Leung (Daiwa); Changlin Liang (Founder & CEO): So would you share what does the future revenue growth rate look like for Dingdong in the future?

Changlin Liang: (Speaking foreign language).

(Translated). In our previous discussion, we highlighted four key drivers for growth. These factors are linked to the organic expansion of our fresh food supply chain capabilities. We’re confident that in the future, these four growth drivers will be able to expand to the same scale as our current business lines or even greater.

Additionally, we have divided Dingdong’s initial development into two stages. The first stage covers the 7-year period from our business's establishment in 2017 to the present, representing the transition from zero to one. During this time, we have achieved profitability and have reached an annual revenue scale of more than 20 billion RMB. Looking ahead, the second stage will encompass the next 7 years, representing the transition from 1 to 10, and we aim to achieve an annual revenue scale of 100 billion RMB. Thank you.

p. 7 · Read in context →

Station unit economics: ~RMB40m capex for 80 stations, breakeven at 500 orders/day, 3–6 month ramp.

Yang Bai (CICC); Song Wang (CFO): Will that increase pressure on the company’s cash flow? […] We estimate that the total CapEx investment for these 80 new stations will be around RMB40 million. Therefore, we have enough self-owned funds to complete their opening without impacting our daily operating funds at all. […] We estimate that the new frontline fulfillment stations in Jiangsu, Zhejiang, and Shanghai can achieve operational breakeven with only 500 orders daily per station. The ramp-up period is about 3 to 6 months. […] Our new frontline fulfillment stations processed an average of 800 orders daily in the first half of this year, and most of them are now breaking even at the operational level.

p. 7 · Read in context →

Q4 FY2023 Earnings Call — Q4 FY2023

The first full year of non-GAAP profit, how private label drives category margins, and the reasoning behind the first buyback. · Open the full transcript →

The full-year milestone: first-ever annual non-GAAP profit on ~RMB20bn revenue, RMB22bn GMV.

Changlin Liang (Founder & CEO): As we consistently implemented our development strategy of efficiency first, with due consideration of scale, we not only achieved non-GAAP profitability for the fifth consecutive quarter, but also marked our first full year of non-GAAP profitability. […] For the full year, our revenue was 19.97 billion RMB, with a GMV of 21.97 billion RMB. Our gross profit margin was 30.7%, and our non-GAAP net profit margin was 0.2%.

p. 2 · Read in context →

How private label drives margin: three brands past 50% of category GMV, with names and repurchase rates.

Changlin Liang (Founder & CEO): Over the past 3 years, we have successfully launched private-label products across three major categories: prepared meals, pork, and soy products, and these three categories of our private labels penetrated over 50% of GMV in 2023. Let me share some examples. First is Cai Chang Qing, a private-label product specializing in prepared home-cooked meals. In 2023, GMV totaled approximately [840] million RMB, a significant increase of 43% from 2022.

In the fourth quarter of 2023, the average number of monthly repurchasing users reached 37%, showcasing the brand's popularity among its customers.

p. 3 · Read in context →

Capital allocation: the US$20m buyback rationale — undervalued stock, ample cash.

Jiajing Chen (CICC); Song Wang (CFO): Dingdong recently announced that the company plans to repurchase up to $20 million of its shares by January 2025. Could you give us more color on this?

Song Wang: (Speaking foreign language).

(Translated). Thank you for your question. As you mentioned, we recently announced a stock repurchase plan that will last 1 year, with a total limit of US$20 million. We expect to begin buying back shares once the blackout period ends following earnings. Our stock is significantly undervalued at the current price, especially in view of our long-term growth prospects. Given our ample cash reserves, buying back stock is an effective way to allocate capital, especially when the stock is undervalued. This program will be beneficial for both the company and its shareholders. […] The key to enhancing the company's overall value lies in our ability to continuously improve our operational capabilities, ensuring sustainable and long-term development.

p. 6 · Read in context →

Q3 FY2023 Earnings Call — Q3 FY2023

The landmark profitability call: the first leading player to turn sustainably profitable, why it calls itself a food company rather than a retailer, and the efficiency math behind it. · Open the full transcript →

The milestone that defined the thesis: first of the leading players to reach sustained profitability.

Changlin Liang (Founder & CEO): Non-GAAP net income margin was 0.3%, marking our fourth consecutive quarter of non-GAAP profitability as we continue to prioritize our strategy of “efficiency first, with due consideration of scale”. In addition, we achieved quarterly profitability on a GAAP basis for the second time since Q4 of 2022.

Sustaining profitability over the past 4 consecutive quarters on a non-GAAP basis is critical for both Dingdong and the industry. First of all, it indicates that we have successfully navigated the difficult macroeconomic and competitive environment we found ourselves in, with many doubting the sustainability of the sector. Second, it reflects the corporate flexibility and adaptability we maintain. With the market continuing to change rapidly, these attributes will remain critical to our long-term sustainability.

Third, among the leading companies competing in the sector, we are the first to achieve profitability. It was a long and difficult journey to get here, but we stuck to our principles and vision, which kept us on the right path. Lastly, having reached the profitability milestone, we are confidently looking to the future, where we will maintain sustainable long-term growth.

p. 2 · Read in context →

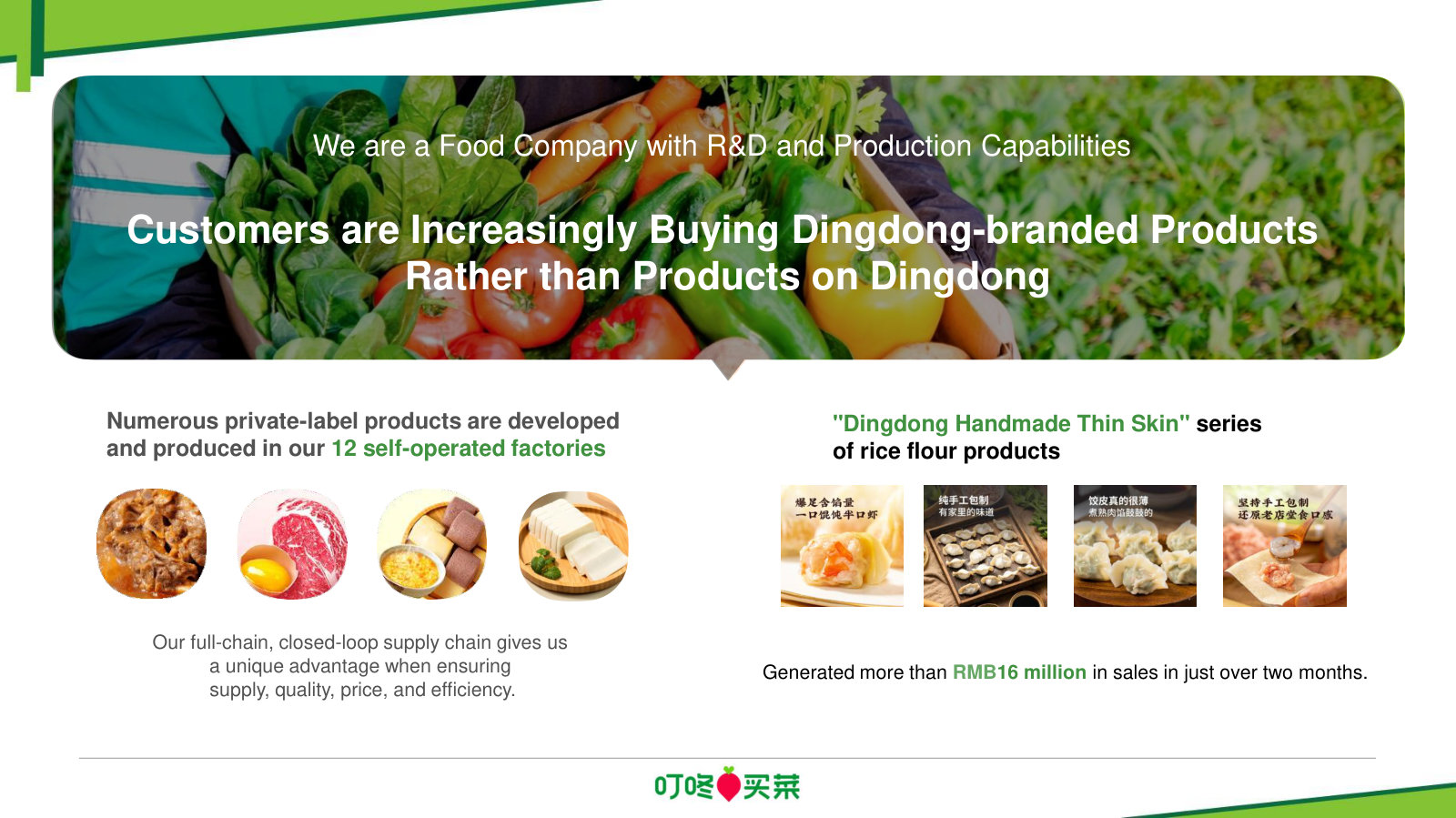

"We are a food company": private-label R&D and 12 self-operated factories, not just a retailer.

Changlin Liang (Founder & CEO): We are more than just a retail company; in fact, we are a food company with R&D and production capabilities. Our top priority has always been to provide our customers with unique, high-quality products. As we grow, our customers are not only buying products on Dingdong, they are increasingly buying Dingdong-branded products. We develop and produce private-label products in 12 self-operated factories in addition to cooperating with high-quality upstream suppliers.

p. 4 · Read in context →

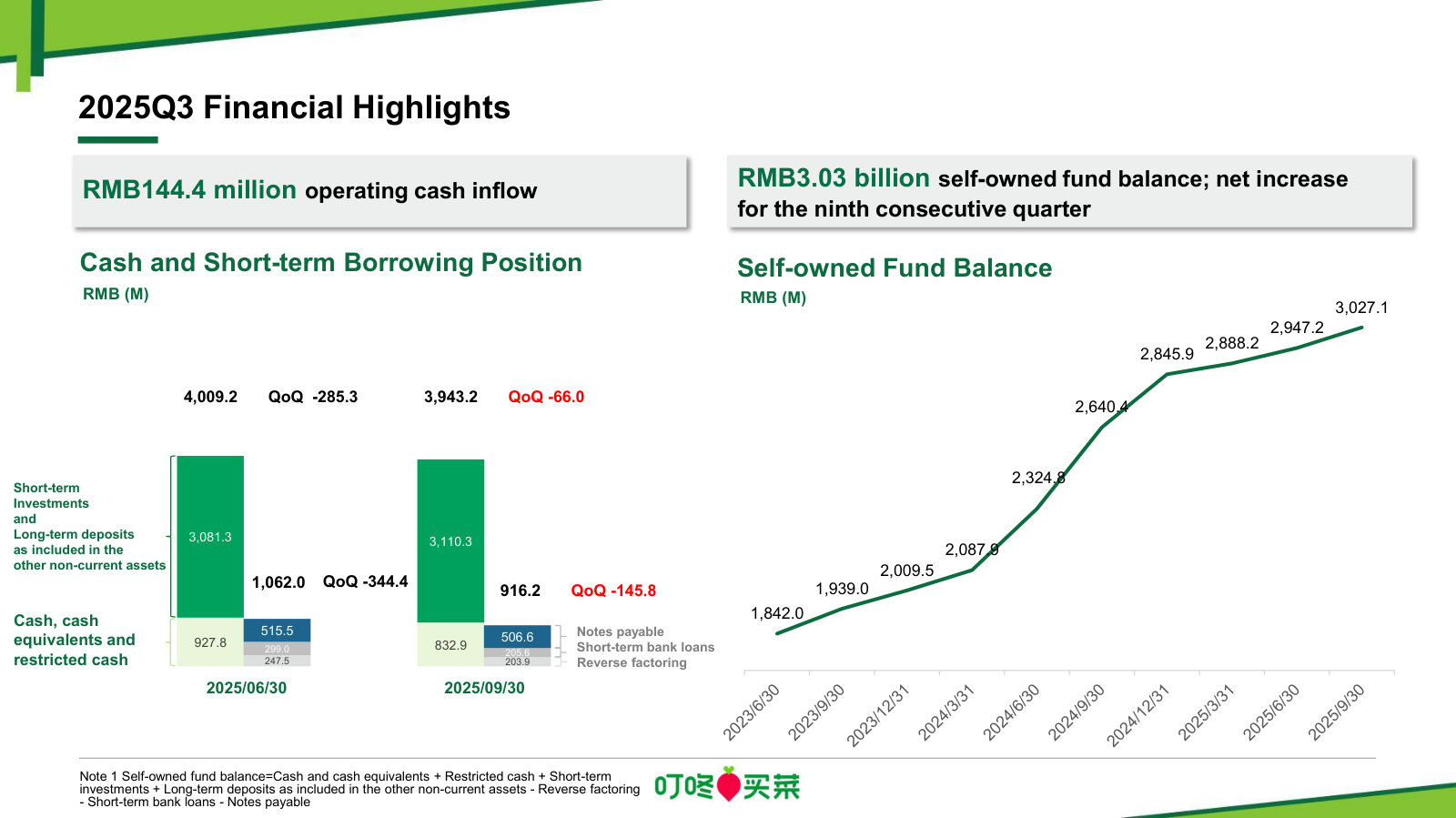

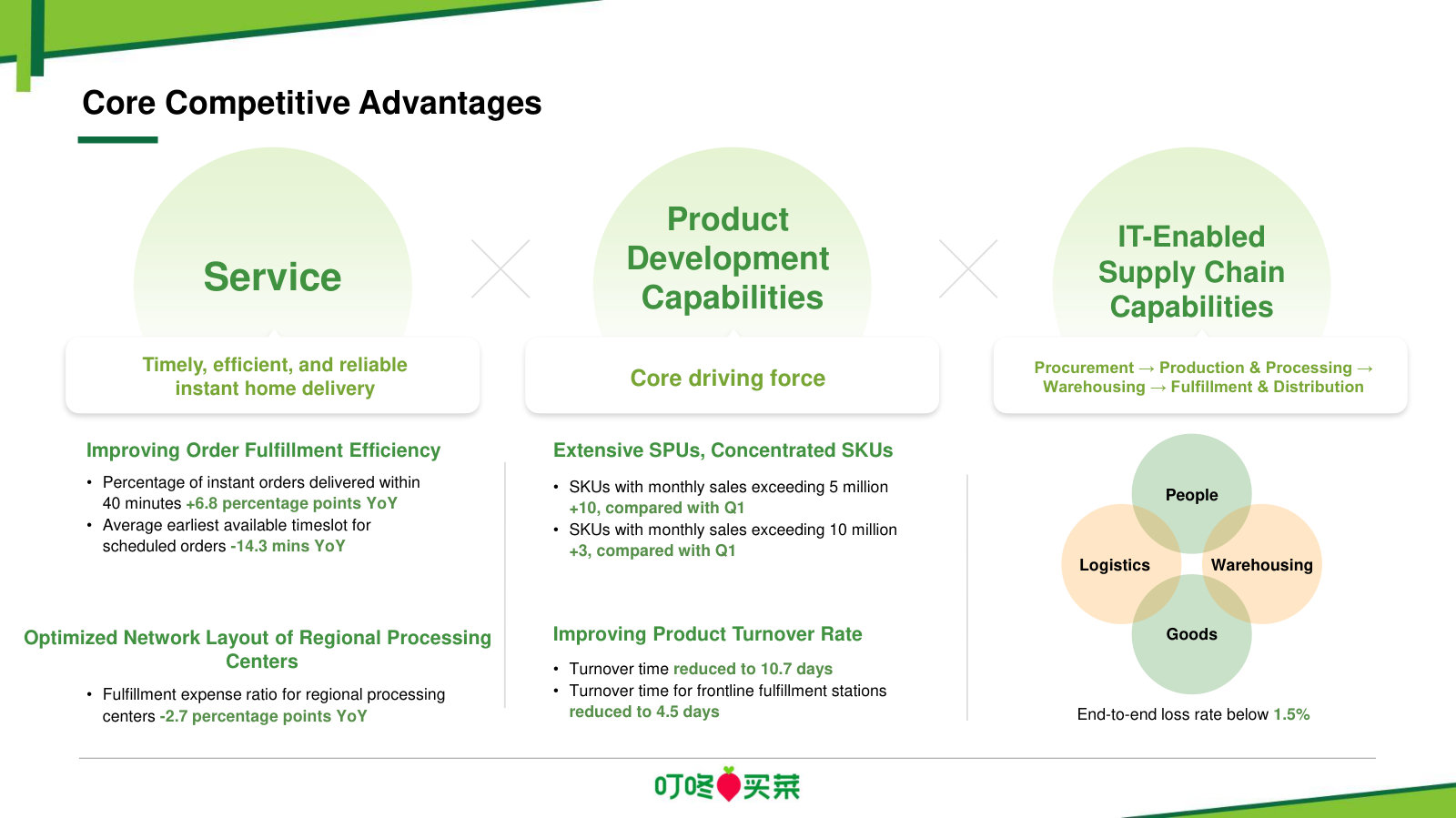

The efficiency engine in numbers: 30.4% gross margin, 10.7-day turnover, <1.5% loss, fulfillment -3.5pts.

Song Wang (Head of Finance): In Q3, gross profit margin increased by 0.4 percentage points year-over-year, reaching 30.4%. This was driven by the continuous improvement of our operational capabilities and efficiency as we expanded along the fresh food supply chain. Our “extensive SPUs, concentrated SKUs” strategy allowed us to leverage our supply chain and product development capabilities to create top-selling products while managing slow-moving ones. This approach also helped us improve supply chain efficiency, resulting in a companywide turnover time of only 10.7 days and 4.5 days for frontline fulfillment stations.

Our end-to-end loss rate was kept below 1.5%. This helped us utilize economies of scale, while improving our bargaining power and optimizing our product mix. As a result, our gross profit margin remains stable while maintaining our ability to provide significant value to our users. […] Our fulfillment expense ratio in Q3 was 23.3%, an improvement of 3.5 percentage points compared to the same period last year, reflecting the substantial impact of this year’s optimization measures.

p. 5 · Read in context →

The competitive-landscape answer: a fractured market that can't be monopolized; low prices from efficiency.

Fiona Fan (Jefferies); Changlin Liang (Founder & CEO): The market for fresh groceries in China is vast and fractured; it cannot be monopolized. As a startup, Dingdong is committed to providing value to consumers. We believe that many different business models can thrive in this market.

As discussed earlier, we believe instant-delivery retail will bring the sector back to the basics of providing efficient service, better product development capabilities, and competitive pricing. In today's world, efficiency and low prices are critical factors that everyone considers when making purchasing decisions. Low prices result from an improvement in efficiency, not a compromise in quality. […] As for fresh grocery products, we continue to work directly with farmers on the ground, cutting out numerous intermediaries in the supply chain. For non-fresh products, we have increased the proportion of private-label products and in-house production to boost our gross profit, while attracting consumers with our exceptional products. In essence, our approach entails improving our product supply, maintaining quality control from the source, meeting a diverse range of user needs, and responding promptly to demand.

p. 7 · Read in context →

Cohort retention as the LTV proof: 2017 users average ~6 orders/month, rising with tenure.

Sophia Chi (Daiwa); Changlin Liang (Founder & CEO): In addition, we have found that the longer customers use our service, the more orders they tend to place. On average, users who joined our platform in 2017 place around 6 orders per month, while the 2018 cohort place 5.4 orders per month. This suggests that our existing users are highly loyal and tend to increase their order frequency over time. We are confident that we will achieve sustained growth by meeting consumer needs and retaining users for longer term.

p. 8 · Read in context →

More calls

Q4 FY2024 Earnings Call — Q4 FY2024 · 3 pages · The Q4 and full-year 2024 results and 2025 outlook — but the only available transcript is paywall-truncated to the cover and intro, so the PDF gives headline framing rather than management's full remarks or Q&A. · Open →

Dingdong (Cayman) Limited's annual reports contain management's most considered account of the business. These are the sections, passages and visual pages worth opening in the originals preserved in Sources.

Dingdong (Cayman) Limited — FY2025 Annual Report (Form 20-F) — FY2025

The latest 20-F, and a pivotal one: it discloses the February 2026 agreement to sell substantially all China operations to Meituan. · Open the full document →

Item 3. Key Information — D. Risk Factors — p. 13 · Read the full section →

The two risks that are specific to this business right now: a mid-flight divestiture to Meituan, and the food-safety exposure inherent to fresh grocery.

The Meituan sale risk: deconsolidation, loss of users/key employees, and a five-year non-compete on To-C grocery in Greater China.

The sale of Dingdong Fresh BVI to the Buyer may adversely affect our business, financial condition or results of operations, our relationships with our current and potential users and employees of Dingdong Fresh BVI, and could result in the loss of our users and key employees. The deconsolidation of Dingdong Fresh BVI after the closing of the Transaction may adversely affect our results of operations and future development strategy. Together with the transaction, we and Mr. Changlin Liang have entered into a five-year non-competition and non-solicitation covenant with the Buyer, which may pose potential restrictions to our To-C fresh grocery e-commerce business within the Greater China region and may adversely affect our relationship wit existing partners and may have an adverse effect on our future growth prospects. After the closing and certain customary matters to be completed, there ca be no assurance that we may achieve anticipated strategic benefits.

p. 16 · Read in context →

Food-safety exposure: a 7+1 quality-control process, but pesticide and heavy-metal residues have slipped through before.

Although we have developed end-to-end quality control procedures through our 7+1 Quality Control Procedure across the entire procurement and fulfillment process, we cannot assure you that we can always identify every quality control issue due to potential flaws, loopholes and bugs of our procedures and human errors, and our efforts to patch up or update our quality control procedures may suffer from delays or failures due to external factors not entirely under our control. In addition, there are inherent limitations in sampling inspection of non-standard products such as fresh produce, seafood meats, which may not identify all the defects and flaws. Our business growth and development, which result in increased cooperation with an increasing number of suppliers and business partners, evolving and increasingly complex supply chain, and continued digitalization of the fulfillment process all possess the potential to exacerbate the pressure on our quality control procedures, which are in turn required to be perfected in a timely manner. We have detected and remedied several cases of sub-par products being sold on Dingdong Fresh, e.g. excessive pesticide or heavy metal residues. Despite our rectification efforts, we are unable to entirely rule out the possibility that similar incidents will take place again in the future.

p. 19 · Read in context →

Item 4. Information on the Company — p. 54 · Read the full section →

Management's own description of the model — a self-operated frontline fulfillment grid and direct-sourced private label — and where the Meituan deal terms are set out.

The deal terms: US$717m cash plus up to ~US$997m total from Meituan's buyer; international business retained; pending SAMR clearance.

On February 5, 2026, we entered into a definitive Share Purchase Agreement (the “Share Purchase Agreement”) with Two Hearts Investments Limited (the “Buyer”), a wholly-owned subsidiary of Meituan (HKEX: 3690). Pursuant to the Share Purchase Agreement, we have agreed to sell to the Buyer all issued and outstanding shares of Dingdong Fresh BVI, which holds through a series of wholly-owned and majority equity interest subsidiaries substantially all of our operations in China (the “Transaction”). The Buyer will pay cash consideration of US$717 million in the Transaction. In addition, we will have the right to receive prior to August 31, 2026 total cash not exceeding US$280 million from Dingdong Fresh BVI and its subsidiaries (provided that the total net cash of Dingdong Fresh BVI and its subsidiaries on a consolidated basis as of December 31, 2025 minus such amounts received by us shall not be less than US$150 million). As such, we expect that it will receive up to US$997 million in cash proceeds from the Transaction. Thi amount is subject to certain adjustments, including those based on certain net cash, net working capital and other financial line item thresholds of Dingdong Fresh BVI and its subsidiaries as of certain agreed upon dates. In the event that the net cash of Dingdong Fresh BVI and its subsidiaries on a consolidated basis as of December 31, 2025 minus the amounts received by us as described above is less than US$150 million, the Buyer has the right to adjust the purchase price cash consideration at closing for any such shortfalls. Our international business is not part of the Transaction and will be retained by us following any necessary reorganizational processes to be completed prior to the closing of the Transaction. As of the date of this annual report, th Transaction has not been completed, and is subject to the satisfaction or waiver of various customary conditions set forth in the Share Purchase Agreement, including the receipt of anti-monopoly clearance from the SAMR.

p. 54 · Read in context →

Scale and the 2021 pivot to “efficiency first” — GMV of RMB26.4bn and thirteen straight non-GAAP-profitable quarters.

As a result, we have achieved significant scale in our business, and accumulated a massive and highly active user base. Our GMV increased from RMB21,969.3 million in 2023 to RMB25,557.4 million in 2024, and further increased to RMB26,436.2 million (US$3,780.3 million) in 2025. Starting from the third quarter of 2021, we strategically shifted our focus to “efficiency first with due consideration of scale”, aiming to achieve profitability to maximize our investors’ interests in us. Ever since our strategic shift, we have been focusing on further strengthening our product competitiveness while optimizing our fulfillment network, so as to increase user stickiness and secure their loyalty with us. Guided by the strategy, we have achieved non-GAAP profitability for thirteen consecutive quarters and GAAP profitability for eight consecutive quarters.

p. 55 · Read in context →

Item 5. Operating and Financial Review and Prospects — p. 85 · Read the full section →

Where management explains a thin-margin scale business: revenue growth drivers and the cost ratios that decide whether it makes money.

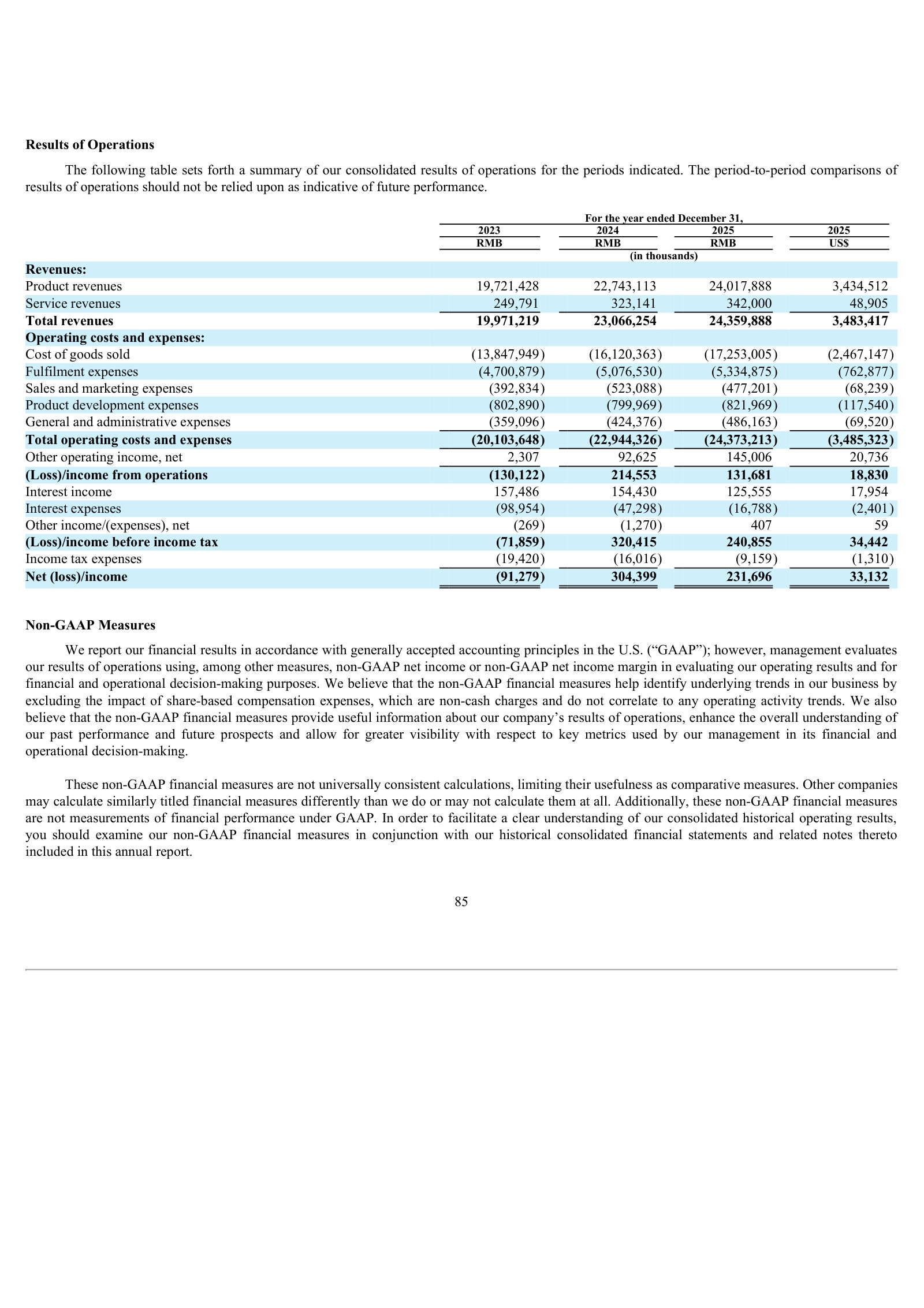

What drove FY2025 revenue (+5.6%): more orders, higher order frequency, new East-China stations, and growing overseas B2B.

Our revenues increased from RMB23,066.3 million in 2024 to RMB24,359.9 million (US$3,483.4 million) in 2025.

Product revenues. Product revenues increased from RMB22,743.1 million in 2024 to RMB24,017.9 million (US$3,434.5 million) in 2025, mainl due to the rise of number of orders resulting from rise in the average monthly number of transacting users and higher monthly order frequency, and new opened frontline fulfillment stations with density and market penetration improved in East China. Additionally, our B2B revenue achieved year-over-year growth, with the revenue contribution from overseas B2B operations continuing to increase and posting rapid sequentially

p. 91 · Read in context →

Item 5. Critical Accounting Policies, Judgments and Estimates — p. 94 · Read the full section →

Gross-basis revenue recognition is why RMB24bn flows through the P&L — it defines Dingdong as a first-party retailer that owns inventory, not a marketplace.

Revenue booked gross because Dingdong is the principal — it fulfills the goods, takes inventory risk, and sets prices.

We recognize product sales made through Dingdong Fresh APP, mini-programs and third-party platforms on a gross basis because we are acting as the principal in these transactions as we (i) are responsible for fulfilling the promise to provide the specified goods, (ii) take on inventory risks and (iii) have discretion in establishing price.

p. 95 · Read in context →

More annual reports

Dingdong (Cayman) Limited — FY2024 Annual Report (Form 20-F) — FY2024 · 201 pages · The pre-divestiture baseline: first full year of GAAP profitability with the China grocery network still fully intact. · Open →

Dingdong (Cayman) Limited — FY2023 Annual Report (Form 20-F) — FY2023 · 192 pages · Shows the “efficiency first” retrenchment year — network pruning and cost discipline on the road to profitability. · Open →

Dingdong (Cayman) Limited — FY2022 Annual Report (Form 20-F) — FY2022 · 178 pages · The strategic-shift year: management reframes from scale-at-all-costs growth to profitability after the Q3 2021 pivot. · Open →

Dingdong (Cayman) Limited — FY2021 Annual Report (Form 20-F) — FY2021 · 352 pages · The first 20-F after the June 2021 NYSE IPO — the original scale-first growth story before the profitability pivot took hold. · Open →

Source: S&P Capital IQ consensus via Xpressfeed · Generated 2026-07-19.

Street snapshot

Three analysts cover the stock and all are constructive — two Buy and one Outperform — for a consensus recommendation score of about 1.33. Their CNY target prices run from 20.69 to 24.19, with a mean of 22.73 and a median of 23.31.

Currency: CNY · Scale: money in millions, absolute (per share) · Analyst counts shown explicitly; recommendation respondents: 3.

| Street view | Reading | Analysts |

|---|---|---|

| Recommendation mix | Buy 2, Outperform 1, Hold 0, Underperform 0, Sell 0 | 3 |

| Consensus score | 1.33 | 3 |

| Target price | mean 22.73; high 24.19; low 20.69 | 3 |

Forward table

Gross margin is held near 29–30% throughout, and coverage thins in the outer years, down to a single estimate for FY2028.

Currency: CNY · Scale: money in millions, absolute (per share) · Analyst count is the estimate count for each period and metric.

| Period | Metric | Mean | YoY | Analysts | Low / high |

|---|---|---|---|---|---|

| FY0E | Revenue | 26,965 | 10.7% | 2 | 25,847 / 28,083 |

| FY0E | EBITDA | 389.0 | 26.4% | 1 | 389.0 / 389.0 |

| FY0E | EBIT | 390.0 | 68.2% | — | — / — |

| FY0E | Net income (GAAP) | 395.0 | 76.2% | 2 | 370.0 / 420.0 |

| FY0E | Net income (normalized) | 492.5 | 39.3% | — | — / — |

| FY0E | EPS (GAAP) | 1.57 | 137.9% | 1 | 1.57 / 1.57 |

| FY0E | EPS (normalized) | 2.19 | 145.5% | 2 | 2.04 / 2.33 |

| FY0E | Gross margin | 29.5% | 1.2% | — | — / — |

| FY0E | Capital expenditure | -40.00 | -19.2% | — | — / — |

| FY0E | ROE | 32.8% | -1.3% | — | — / — |

| FY0E | Cash from operations | 819.0 | 24.8% | — | — / — |

| FY+1E | Revenue | 29,038 | 7.7% | 2 | 27,280 / 30,796 |

| FY+1E | EBITDA | 459.0 | 18.0% | 1 | 459.0 / 459.0 |

| FY+1E | EBIT | 469.5 | 20.4% | — | — / — |

| FY+1E | Net income (GAAP) | 477.0 | 20.8% | 2 | 464.0 / 490.0 |

| FY+1E | Net income (normalized) | 582.5 | 18.3% | — | — / — |

| FY+1E | EPS (GAAP) | 1.96 | 24.8% | 1 | 1.96 / 1.96 |

| FY+1E | EPS (normalized) | 2.58 | 17.8% | 2 | 2.48 / 2.67 |

| FY+1E | Gross margin | 29.4% | -0.3% | — | — / — |

| FY+1E | Capital expenditure | -46.00 | 15.0% | — | — / — |

| FY+1E | Cash from operations | 856.0 | 4.5% | — | — / — |

| FY+1E | ROE | 27.7% | -15.5% | — | — / — |

| FY+2E | Revenue | 28,245 | -2.7% | 1 | 28,245 / 28,245 |

| FY+2E | EBIT | 566.0 | 20.6% | — | — / — |

| FY+2E | Net income (GAAP) | 513.0 | 7.5% | 1 | 513.0 / 513.0 |

| FY+2E | Net income (normalized) | 604.0 | 3.7% | — | — / — |

| FY+2E | EPS (normalized) | 2.79 | 8.3% | 1 | 2.79 / 2.79 |

| FY+2E | Gross margin | 29.6% | 0.7% | — | — / — |

| FY+2E | Capital expenditure | -30.00 | -34.8% | — | — / — |

| FY+2E | Cash from operations | 737.0 | -13.9% | — | — / — |

| Q2 FY2026 | Revenue | 6,902 | 15.5% | 1 | 6,902 / 6,902 |

| Q2 FY2026 | EBIT | 81.00 | 5.2% | — | — / — |

| Q2 FY2026 | Net income (GAAP) | 96.00 | -8.3% | 1 | 96.00 / 96.00 |

| Q2 FY2026 | Net income (normalized) | 123.0 | 2.5% | — | — / — |

| Q2 FY2026 | Gross margin | 29.2% | 0.7% | — | — / — |

| Q3 FY2026 | Revenue | 7,721 | — | 1 | 7,721 / 7,721 |

| Q3 FY2026 | EBIT | 130.0 | — | — | — / — |

| Q3 FY2026 | Net income (GAAP) | 140.0 | 74.3% | 1 | 140.0 / 140.0 |

| Q3 FY2026 | Net income (normalized) | 171.0 | — | — | — / — |

| Q3 FY2026 | Gross margin | 29.4% | — | — | — / — |

| Q4 FY2026 | Revenue | 7,112 | 13.9% | 1 | 7,112 / 7,112 |

| Q4 FY2026 | EBIT | 71.00 | -1.4% | — | — / — |

| Q4 FY2026 | Net income (GAAP) | 87.00 | 180.7% | 1 | 87.00 / 87.00 |

| Q4 FY2026 | Net income (normalized) | 116.0 | 7.4% | — | — / — |

| Q4 FY2026 | Gross margin | 29.4% | 0.7% | — | — / — |

Estimate momentum

Forward consensus has been broadly stable. The moves are small and rest on thin outer-year coverage.

Currency: CNY · Scale: money in millions, absolute (per share) · Point-in-time consensus; analyst count is shown where supplied.

| Period | Metric | Lookback | Then | Now | Direction / magnitude | Analysts |

|---|---|---|---|---|---|---|

| 2027 | Revenue | 30d | 29,038 | 29,038 | flat 0.0% | — |

| 2027 | Revenue | 90d | 29,763 | 29,038 | down 2.4% | — |

| 2027 | Revenue | 180d | 29,387 | 29,038 | down 1.2% | — |

| 2027 | EPS (normalized) | 30d | 2.58 | 2.58 | flat 0.0% | — |

| 2027 | EPS (normalized) | 90d | 2.57 | 2.58 | up 0.1% | — |

| 2027 | EPS (normalized) | 180d | 2.55 | 2.58 | up 0.9% | — |

| 2028 | Revenue | 30d | 28,245 | 28,245 | flat 0.0% | — |

| 2028 | Revenue | 90d | 28,245 | 28,245 | flat 0.0% | — |

| 2028 | EPS (normalized) | 30d | 2.79 | 2.79 | flat 0.0% | — |

| 2028 | EPS (normalized) | 90d | 2.79 | 2.79 | flat 0.0% | — |

Beat / miss record

Normalized-EPS surprise history is thin: the only captured quarter (Q2 2024) shows an 817% beat, but off a near-zero 0.05 consensus that distorts the figure.

Current sequences by metric: Revenue: 2 consecutive misses; EPS (normalized): 1 consecutive beat.

Currency: CNY · Scale: money in millions, absolute (per share) · Consensus is captured before each actual first became effective; analyst count shown per observation.

| Quarter | Metric | Consensus as of | Actual | Surprise | Outcome | Analysts |

|---|---|---|---|---|---|---|

| Q1 FY2026 | Revenue | 6,348 | 5,893 | -7.2% | Miss | — |

| Q4 FY2025 | Revenue | 6,301 | 6,243 | -0.9% | Miss | — |

| Q2 FY2025 | Revenue | 5,971 | 5,976 | 0.1% | Beat | — |

| Q1 FY2025 | Revenue | 5,470 | 5,479 | 0.2% | Beat | — |

| Q4 FY2024 | Revenue | 5,892 | 5,905 | 0.2% | Beat | — |

| Q3 FY2024 | Revenue | 6,508 | 6,538 | 0.5% | Beat | — |

| Q2 FY2024 | Revenue | 5,425 | 5,599 | 3.2% | Beat | — |

| Q2 FY2024 | EPS (normalized) | 0.05 | 0.46 | 817.2% | Beat | — |

| Q1 FY2024 | Revenue | 4,872 | 5,024 | 3.1% | Beat | — |

Where the street disagrees

Disagreement is widest on EBITDA and outer-year revenue. Near-term revenue, by contrast, is tightly clustered (stddev ~94m on a ~24,288m mean), so the small estimate counts limit how much to read into the wider spreads.

Currency: CNY · Scale: money in millions, absolute (per share) · Dispersion is high-low divided by absolute mean; analyst count shown per item.

| Period | Metric | Mean | Low | High | Spread / mean | Analysts |

|---|---|---|---|---|---|---|

| 2025 | EBITDA | 356.3 | 311.4 | 445.5 | 37.6% | 3 |

| 2026 | EPS (normalized) | 2.19 | 2.04 | 2.33 | 13.3% | 2 |

| 2026 | Net income (GAAP) | 395.0 | 370.0 | 420.0 | 12.7% | 2 |

| 2027 | Revenue | 29,038 | 27,280 | 30,796 | 12.1% | 2 |

| 2025 | Net income (GAAP) | 268.6 | 253.0 | 280.0 | 10.1% | 4 |

Source: Visible Alpha consensus via S&P Xpressfeed · Consensus as of 2026-06-25 · generated 2026-07-19.

Model trust

With only one contributor this cannot be read as broad consensus, and the freshest line-item revision is November 2025 while the core P&L and KPI lines were last touched in August 2025, both stale against this July 2026 snapshot. Treat it as a single-analyst view rather than the market's.

Base currency: CNY · VA scales normalized from Abs, M; item currencies and units retained · Coverage depth and vintage; broker count is the maximum represented.

| Brokers | Line items | Last revision |

|---|---|---|

| 1 | 329 | 2026-06-25 |

Caution: Coverage is thin at 1 broker.

Operating KPIs

The most decision-useful company-specific drivers with full forward coverage are GMV, total orders, average order value and the fulfillment-station count. Monthly-active-user coverage stops after FY-2026, so the user base is only partly modeled.

Base currency: CNY · VA scales normalized from Abs, M; item currencies and units retained · FY-1A / FY0E / FY+1E; broker count shown per KPI.

| Operating KPI | Source | FY-1A | FY0E | FY+1E | Brokers |

|---|---|---|---|---|---|

| (Increase)/decrease in inventories | CD | -270,918.87bn Amount | -213,831.34bn Amount | -446.47bn Amount | 1 |

| (Increase)/decrease in receivables | CD | 17,074.74bn Amount | 16,302.88bn Amount | 13,242.04bn Amount | 1 |

| (Increase)/decrease in working capital | CD | -471,388.24bn Amount | 500,313.64bn Amount | -587,103.91bn Amount | 1 |

| Accounts payable | CD | 1,529,640.10bn Amount | 2,053,313.78bn Amount | 1,539,409.11bn Amount | 1 |

| Amounts due to related parties - Current | CD | 506,844.06bn Amount | 556,954.16bn Amount | 539,789.18bn Amount | 1 |

| Assets - Noncurrent | CD | 1,774,373.50bn Amount | 1,848,371.00bn Amount | 1,838,868.50bn Amount | 1 |

| Average order value - Non S5 - Product(CNY) | CD | 113.0 Amount | 113.0 Amount | 113.0 Amount | 1 |

| Average order value - S5 - Product(CNY) | CD | 70.00 Amount | 70.00 Amount | 70.00 Amount | 1 |

| Average order value(CNY) | CD | 69.30 Amount | 70.42 Amount | 70.53 Amount | 1 |

| Capital additions | CD | 106,076.01bn Amount | 112,730.50bn Amount | 120,744.41bn Amount | 1 |

| Cash and cash equivalents-Beginning balance | CD | 890,215.00bn Amount | 1,703,279.45bn Amount | 3,623,442.53bn Amount | 1 |

| Cash and cash equivalents-Ending balance | CD | 1,703,279.45bn Amount | 3,623,442.53bn Amount | 4,588,260.10bn Amount | 1 |

P&L bridge

Base currency: CNY · VA scales normalized from Abs, M; item currencies and units retained · Margins are derived against revenue; YoY compares adjacent fiscal columns; broker count shown per line.

| P&L line | FY-1A | FY0E | FY+1E | Brokers |

|---|---|---|---|---|

| Revenue | 24,922,345.78bn Amount | 26,485,805.55bn Amount (6.3% YoY) | 28,368,656.55bn Amount (7.1% YoY) | 1 |

| Gross Profit | 7,286,895.82bn Amount (29.2% margin) | 7,736,090.82bn Amount (29.2% margin; 6.2% YoY) | 8,283,941.22bn Amount (29.2% margin; 7.1% YoY) | 1 |

| Ebitda | 1,251,570.71bn Amount (5.0% margin) | 1,437,277.93bn Amount (5.4% margin; 14.8% YoY) | 1,517,363.89bn Amount (5.3% margin; 5.6% YoY) | 1 |

| Operating Income | 352,982.34bn Amount (1.4% margin) | 482,318.19bn Amount (1.8% margin; 36.6% YoY) | 494,516.96bn Amount (1.7% margin; 2.5% YoY) | 1 |

| Net Income | 401,622.34bn Amount (1.6% margin) | 495,288.19bn Amount (1.9% margin; 23.3% YoY) | 567,486.96bn Amount (2.0% margin; 14.6% YoY) | 1 |

| Eps | 1.80 Amount | 2.22 Amount (23.3% YoY) | 2.54 Amount (14.6% YoY) | 1 |

Consensus dispersion

Every item carries a single contributor, so minimum, maximum and quartiles collapse onto the mean and standard deviation is zero. There is effectively no consensus dispersion to read here; the flat spreads reflect the absence of a second estimate, not genuine analyst agreement.

Base currency: CNY · VA scales normalized from Abs, M; item currencies and units retained · Top high-low spreads relative to absolute mean; requires at least 3 brokers.

| Line item | Period | Mean | Min | Q1 | Q3 | Max | Spread / mean | Brokers |

|---|---|---|---|---|---|---|---|---|

| No qualifying dispersion | — | — | — | — | — | — | — | — |

Quarterly path

Year-over-year revenue growth stays in the mid-single digits; resting on one August-2025 model, the pattern reads as seasonal rather than a genuine inflection.

Base currency: CNY · VA scales normalized from Abs, M; item currencies and units retained · Next four supplied quarters; final column is maximum broker coverage in the row.

| Quarter | (Increase)/decrease in inventories | (Increase)/decrease in receivables | (Increase)/decrease in working capital | Accounts payable | Amounts due to related parties - Current | Total revenue | EPS Diluted, Applicable to common stockholders(CNY) | Broker coverage |

|---|---|---|---|---|---|---|---|---|

| 3QFY-2026 | — | — | — | — | — | 7,088,974.57bn Amount | 0.73 Amount | 1 |

| 4QFY-2026 | — | — | — | — | — | 6,973,876.85bn Amount | 0.72 Amount | 1 |

| 1QFY-2027 | — | — | — | — | — | 6,166,624.62bn Amount | 0.41 Amount | 1 |

| 2QFY-2027 | — | — | — | — | — | 7,049,012.58bn Amount | 0.67 Amount | 1 |

435 stale period values omitted; 8 line items fully removed.

Source: S&P Capital IQ transcripts via Xpressfeed · latest indexed call 2025-11-12 · generated 2026-07-19.

Latest call digest

Dingdong (Cayman) Limited, Q3 2025 Earnings Call, Nov 12, 2025 · 2025-11-12T12:00:00

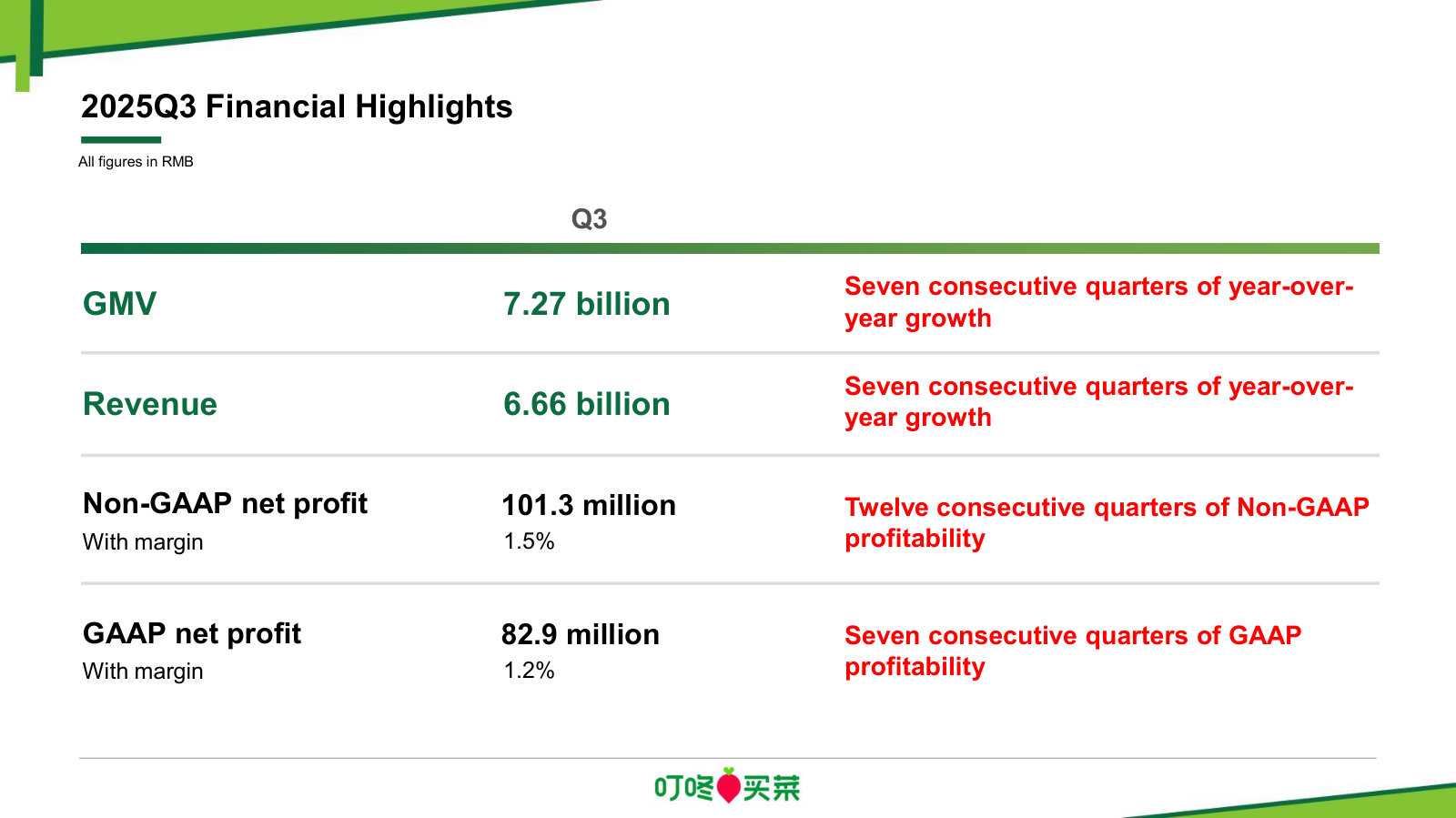

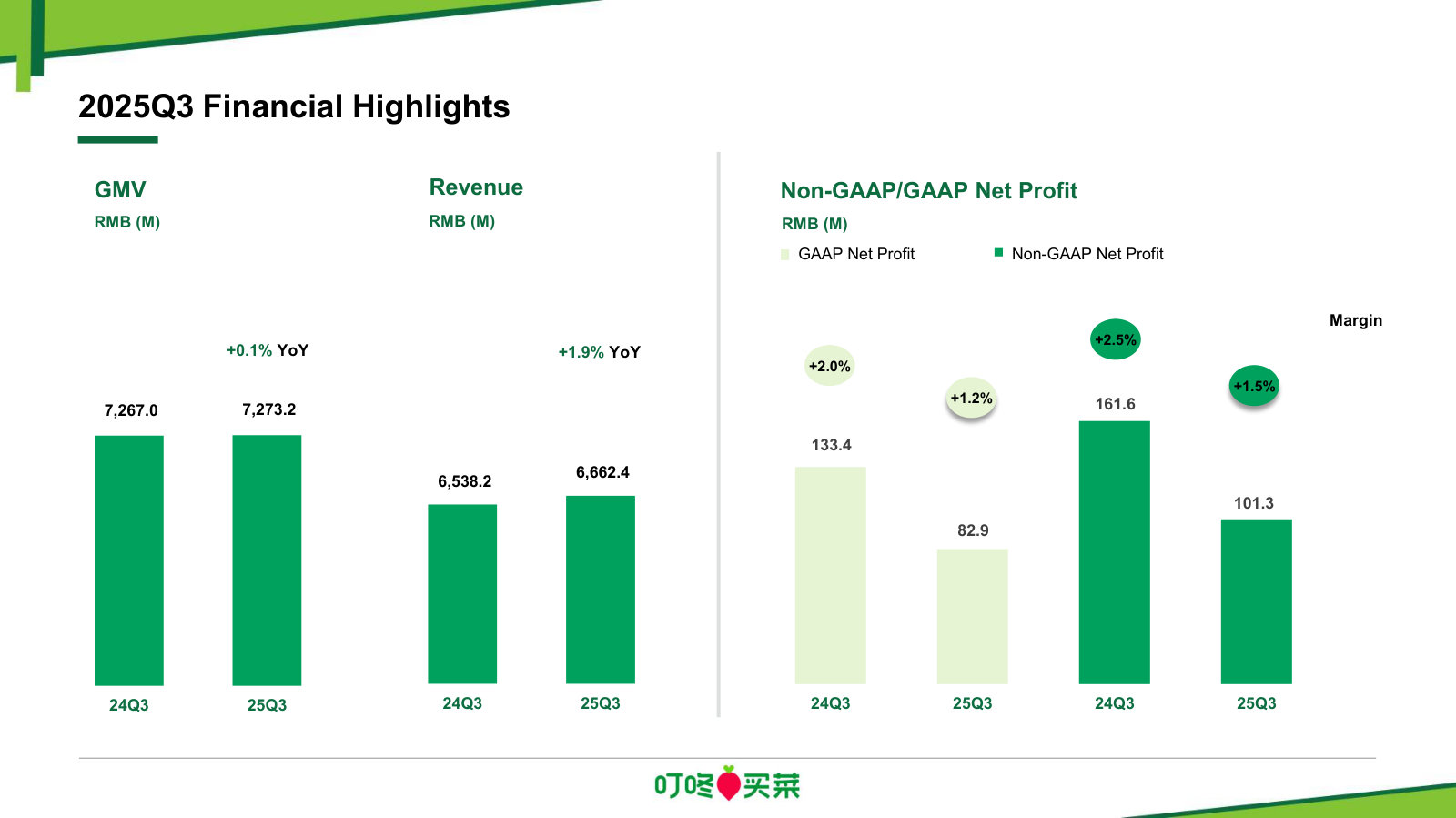

Q3 2025 (reported Nov 12, 2025). The prepared remarks led with record absolutes: GMV of RMB 7.27 billion and revenue of RMB 6.66 billion, described as Dingdong's highest ever, alongside a 12th straight quarter of non-GAAP profitability and a 7th of GAAP profitability. But the growth underneath is now essentially flat — GMV up 0.1% and revenue up 1.9% year-over-year — a sharp step down from the ~27% revenue growth reported a year earlier in Q3 2024. Management used the call to unveil a new "One Big, One Small, One World" framework (high-volume top-selling products; frontline stations in small cities; international expansion) layered on top of the existing 4G strategy. Profitability also compressed: non-GAAP net margin was 1.5% (vs. a 2.5% Q3 2024 peak) and gross margin 28.9%, down 0.9 percentage points. The Q&A reality was thin and did not test the deceleration: Jefferies' line was initially muted, and only two questions landed — CICC on the competitive landscape and Jefferies on the top-selling product strategy — both of which management answered on its own terms, reiterating a differentiation-over-price-war posture. The Q4 outlook was the softest in the recent history reviewed: management guided only to maintaining last year's scale (i.e., flat) and non-GAAP profitability.

Participant coverage from the latest call.

| Group | Participants | Count |

|---|---|---|

| Management | Operator; Nicky Zheng — Director of Investor Relations, Dingdong (Cayman) Limited; Liang Changlin — Founder & Chairman, Dingdong (Cayman) Limited; Song Wang — CEO & Director, Dingdong (Cayman) Limited | 4 |

| Analysts | Yang Bai — Analyst, China International Capital Corporation Limited, Research Division; Unknown Analyst | 2 |

Curated latest-call exchanges; one row per analyst topic.

| Analyst | Firm | Topic | What changed in Q&A |

|---|---|---|---|

| Yang Bai | China International Capital Corporation Limited, Research Division | Competitive landscape in instant retail / fresh groceries | Asked how Dingdong views intensifying competition from Alibaba and Meituan and what opportunities it creates; Liang reframed to long-term differentiation and supply-chain depth rather than price competition, and did not quantify any share impact. |

| Erica Chua | Jefferies LLC, Research Division | Top-selling product strategy and summer campaign | After an initial muted line, asked management to elaborate on the top-selling product strategy tied to the Q3 summer campaign; Liang cited specific blockbuster SKUs and the shift from a channel-distributor to a product-manager mindset. |

Theme tracker

Themes are curator-classified across supplied calls.

| Theme | Status | Quarters mentioned | Read-through |

|---|---|---|---|

| Competition and price wars in instant retail | persisted | Q4 2022, Q1 2023, Q3 2023, Q2 2024, Q2 2025, Q3 2025 | Analysts have raised the competitive landscape almost every year; management's answer is consistent — decline to name or quantify rivals and pivot to its 'narrow and deep' differentiation. By Q3 2025 the tone shifted to openly acknowledging that competition is intensifying. |

| 4G strategy (good users, products, services, mind share) | emerged | Q4 2024, Q1 2025, Q2 2025, Q3 2025 | Framed as 'better' in Q4 2024 and formally launched in Q1 2025; now the organizing narrative of every call. Management ties it to the quality pivot that has compressed near-term growth and margins. |

| International / overseas expansion | emerged | Q2 2024, Q1 2025, Q2 2025, Q3 2025 | Grew from a brief mention in 2024 to a named pillar ('One World') by Q3 2025, anchored on supply-chain export partnerships (DFI, FairPrice, Lee Kum Kee) rather than replicating the domestic station model abroad. |

| Full-chain AI integration | emerged | Q2 2025, Q3 2025 | Introduced as a dedicated segment of prepared remarks in Q2 2025 (supply-chain intelligence, LLM agents, consumer app features) and referenced again in Q3 2025; still a new and thinly evidenced theme. |

| Pandemic / high-base year-over-year effects | dropped | Q4 2022, Q1 2023, Q2 2023, Q3 2023, Q4 2023, Q1 2024 | Dominated commentary through 2023 as the explanation for declining year-over-year revenue; fully absent from 2025 calls once comparisons normalized. Its disappearance marks the transition out of the post-COVID base distortion. |

| Supply-chain depth, self-operated factories and Guyu / private label | persisted | Q4 2022, Q4 2023, Q3 2024, Q4 2024, Q1 2025, Q2 2025, Q3 2025 | The most durable strategic thread — direct sourcing, in-house factories and the Guyu food group are presented as the moat in every call, and are the single most-questioned topic in Q&A. |

| Frontline fulfillment station expansion | persisted | Q2 2024, Q3 2024, Q4 2024, Q1 2025, Q3 2025 | Station-opening targets were a 2024 growth driver (80, raised to 110, ended at 130). In 2025 the emphasis shifted to smaller-city stations (40 opened year-to-date, 17 in Q3 2025), reflecting the search for new penetration as core-region growth slows. |

Guidance ledger

Quotes, calls, and speakers are source-verified; outcomes are curator-classified.

| Verbatim guidance | Call | Speaker | Curator outcome | Outcome note |

|---|---|---|---|---|

| “we are increasing our target for new fulfillment stations openings in 2024 to approximately 110.” | Dingdong (Cayman) Limited, Q3 2024 Earnings Call, Nov 06, 2024 · 2024-11-06T12:00:00 | Liang Changlin | kept | The Q4 2024 call reported 130 new frontline fulfillment stations opened during the year, surpassing the raised 110 target. |

| “we aim to achieve an annual revenue scale of RMB 100 billion.” | Dingdong (Cayman) Limited, Q2 2024 Earnings Call, Aug 07, 2024 · 2024-08-07T12:00:00 | Liang Changlin | pending | A long-term ambition framed over the next seven years (a '1 to 10' stage); FY2024 revenue was RMB 23.07 billion and growth has since decelerated, so the target remains far out and unproven in the available history. |

| “We expect to achieve year-over-year scale growth and maintain non-GAAP profitability in the first quarter of 2025.” | Dingdong (Cayman) Limited, Q4 2024 Earnings Call, Mar 06, 2025 · 2025-03-06T12:00:00 | Liang Changlin | kept | Q1 2025 revenue rose 9.1% year-over-year with non-GAAP net profit of RMB 30 million. |

| “We anticipate maintaining year-on-year growth in scale and achieving non-GAAP profitability for the second quarter of 2025.” | Dingdong (Cayman) Limited, Q1 2025 Earnings Call, May 16, 2025 · 2025-05-16T12:00:00 | Liang Changlin | kept | Q2 2025 revenue rose 6.7% year-over-year with non-GAAP net profit of RMB 130 million. |

| “We expect significant growth in both performance scale and profit margin by then.” | Dingdong (Cayman) Limited, Q1 2025 Earnings Call, May 16, 2025 · 2025-05-16T12:00:00 | Liang Changlin | pending | Refers to the end of 2025. On the available history, Q3 2025 revenue growth had slowed to 1.9% and Q4 was guided only to flat scale, so a significant second-half step-up in scale and margin is not yet evident. |

| “we still aim for a stable scale year-over-year and maintain non-GAAP profitability.” | Dingdong (Cayman) Limited, Q2 2025 Earnings Call, Aug 21, 2025 · 2025-08-21T12:00:00 | Liang Changlin | kept | Q3 2025 GMV was roughly flat (+0.1%), revenue rose 1.9%, and non-GAAP profitability was maintained (12th consecutive quarter). |

| “We anticipate that export revenues this year will reach RMB 600 million and expect that by 2027, exports will account for more than 50% of Guyu's revenues.” | Dingdong (Cayman) Limited, Q1 2025 Earnings Call, May 16, 2025 · 2025-05-16T12:00:00 | Song Wang | pending | Both the full-year 2025 export figure and the 2027 mix target fall outside the available call history and cannot be verified here. |

| “maintaining last year's scale and non-GAAP profitability in Q4.” | Dingdong (Cayman) Limited, Q3 2025 Earnings Call, Nov 12, 2025 · 2025-11-12T12:00:00 | Liang Changlin | pending | Q4 2025 results are not yet in the call history; this guides only to flat year-over-year scale. |

Q&A pressure map

Question counts and firms are curator tallies; analyst coverage shown above.

| Topic | Questions | Firms | Pressure / response |

|---|---|---|---|

| Product development, private label and self-operated factories (Guyu) | 8 | Jefferies LLC, Research Division, China International Capital Corporation Limited, Research Division, Daiwa Securities Co. Ltd., Research Division, Crédit Suisse AG, Research Division | The single most recurring Q&A theme across the twelve calls. Management engages fully, answering with detailed product examples (Black Diamond pork, Guyu food group, summer top-sellers) rather than deflecting. |

| Competitive landscape | 6 | Jefferies LLC, Research Division, China International Capital Corporation Limited, Research Division, Daiwa Securities Co. Ltd., Research Division | Pressed repeatedly since 2023. Management consistently declines to name or size specific rivals or their impact on Dingdong, redirecting to its own differentiation — a soft, if consistent, deflection. |

| Cash flow, short-term borrowings and balance sheet | 4 | China International Capital Corporation Limited, Research Division, CMS | Concentrated in 2023-2024 as profitability and cash turned positive. The CFO answers these directly with specific figures on operating cash flow, net debt and self-owned funds; no evasion evident. |

| 4G strategy execution | 2 | Jefferies LLC, Research Division | A newer line of questioning in 2025 as the quality pivot began weighing on growth; management frames it as a deliberate, transitional inside-out transformation. |

Language shifts

Only language evidence verified against the referenced component is shown.

| Observation | Verbatim evidence | Call ID | Component |

|---|---|---|---|

| Peak confidence in the 2024 calls — management layered a forward-looking superlative onto already strong guidance, the high-water mark of tone in this history. | “We have full confidence in the growth of scale and profits this year and we are even more confident about the future.” | 1887550005 | 2 |

| First explicit hedge that the strategy shift could hurt near-term results, introduced in Q4 2024 after a year of uniformly upbeat outlooks — a new note of caution. | “we're also in the process of transitioning from pursuing short-term scale and profitability, so focusing on quality and long-term competitiveness, which may impact us.” | 1933226862 | 2 |

| Guidance language stepped down from 'growth' to merely 'stable scale' by Q2 2025, an explicit lowering of the near-term growth bar versus the 2024 confidence. | “we still aim for a stable scale year-over-year and maintain non-GAAP profitability.” | 1957230433 | 2 |

| By Q3 2025 management openly characterized competition as intensifying — more pointed than the earlier detached 'we rarely evaluate our peers' framing. | “Industry-wide competition in the instant retail sector is intensifying with both platforms and off-line merchants increasing their investments to gain market share.” | 1969787743 | 2 |

The twelve-call arc is coherent: a hard-won 2023 turn to profitability, a high-growth 2024, and a 2025 in which the 4G quality pivot has preserved the profit streak and cash generation but flattened growth to roughly zero and compressed margins from their 2024 peak. The debate the calls sharpen is whether 'narrow and deep' differentiation can reaccelerate scale as instant-retail competition intensifies, or whether flat top-line with steady low-single-digit margins is the new steady state.

Fresh Grocery, Net Cash

Dingdong is a self-operated fresh-grocery delivery company in China that IPO'd on the NYSE in June 2021 at US$23.50 per ADS, burned through more than ¥13 billion becoming a scale player, and then retrenched. It now posts modest GAAP profits and positive free cash flow on ¥24.4 billion of revenue, and holds ¥3.98 billion (about US$569 million) of cash and short-term investments — close to its entire market value. This report examines whether that combination is a margin of safety or a value trap.

Dingdong reports its financials in Chinese renminbi (¥); its shares trade in US dollars (US$) on the NYSE as American Depositary Shares (ADSs). Figures below are in ¥ unless marked US$. US$ equivalents shown in parentheses are the company's own conversions from its filings (roughly ¥7.0 per US$1).

What the company does

Dingdong runs an on-demand grocery platform built on a grid of company-operated frontline fulfillment stations — micro-warehouses placed inside dense neighborhoods that stock fresh food and dispatch it to a customer's door, typically within about half an hour. It is not a marketplace: the company sources, stocks, prices, and delivers the goods itself, selling vegetables, meat, seafood, fruit, eggs, and prepared food. At the time of its IPO it operated more than 950 such stations across 29 cities [1].

The model is capital-light in equipment but operationally heavy: gross margins run near 30%, and the business earns its keep by converting orders densely enough that delivery and station costs stay below that gross margin. Average order value was ¥70.1 in 2025 [2]; gross merchandise value (GMV) reached ¥26.4 billion (US$3.78 billion) [3]. After its retrenchment, the footprint is concentrated in the Yangtze River Delta — Jiangsu, Zhejiang, and Shanghai — where the company added 61 net new stations and entered three new cities in 2025 [4].

FY2025 Revenue (¥bn)

FY2025 Net Income (¥m)

FY2025 Free Cash Flow (¥m)

Cash and Investments (¥bn)

Sources: FY2025 revenue, net income, GMV — FY2025 Annual Report, Operating and Financial Review [5]; cash and short-term investments [6]; free cash flow derived from reported operating cash flow of ¥535.5m less capex of ¥177.8m [7].

From blitzscale to profit

Dingdong's history divides cleanly at the third quarter of 2021, when management shifted its strategy to "efficiency first, with due consideration of scale" [8]. Before that pivot, the company grew revenue from ¥11.3 billion in 2020 [9] to ¥24.2 billion in 2022 while losing enormous sums — a ¥6.4 billion net loss in 2021 alone [10], equal to a 32% net loss margin [11]. Those years built the platform and left an accumulated deficit of roughly ¥13 billion still sitting on the balance sheet today.

The retrenchment was deliberate. In 2022 and 2023 the company withdrew from cities with immaterial GMV that required heavy investment to scale [12], and revenue fell 17.5% to ¥20.0 billion in 2023. That was the cost of the turn: it produced the first full year of non-GAAP profit in 2023, the first GAAP profits in 2024 and 2025, and a return to top-line growth.

Source: 2023–2025 figures per FY2025 Annual Report, Operating and Financial Review [13]; 2021–2023 figures per FY2023 Annual Report [14]; 2020–2022 figures per FY2022 Annual Report [15].

The profit inflection is the more important chart. Net losses of ¥6.4 billion (2021) and ¥806.9 million (2022) narrowed to ¥91.3 million in 2023, then flipped to net income of ¥304.4 million in 2024 and ¥231.7 million (US$33.1 million) in 2025 [16] — net margins of 1.3% and 1.0% [17]. By its own account the company has now delivered GAAP profits for eight straight quarters and positive year-over-year revenue growth for eight straight quarters [18].

Source: FY2022, FY2023, and FY2025 Annual Reports, Financial Highlights [19] [20] [21].

Two features of the profit deserve to be held in view rather than celebrated. The margin is thin — a 1.0% net margin means a small move in gross margin or fulfillment cost swings the whole result — and growth has decelerated sharply, from a 46% revenue CAGR through 2022 to 5.6% in 2025 [22], partly because falling consumer prices for staples like pork and vegetables weighed on revenue. This is a business that has stabilized, not one visibly compounding.

The Balance Sheet

What makes Dingdong unusual is not its income statement but its capitalization. At the end of 2025 the company held ¥3.98 billion (US$568.7 million) in cash, restricted cash, and short-term investments [23], against ¥0.87 billion (US$124.6 million) of short-term borrowings that management has been actively reducing [24]. That leaves net cash near ¥3.1 billion (about US$444 million) — a figure the company itself computes by netting short-term borrowings against its cash, restricted cash, short-term investments, and long-term deposits [25].

The market's own valuation sits against that. With roughly 354 million ordinary shares outstanding [26] — each ADS represents 1.5 ordinary shares [27] — a recent ADS price near US$2.58 (April 2026, a market value rather than a figure from the filings) implies a market value of about US$609 million. At that price the ~US$609 million market value sits modestly above the ¥3.98 billion (US$568.7 million) of cash and investments; only at the lower prices the stock has traded through does the equity change hands at or below that cash. The equity trades in the vicinity of its net cash either way, and the business itself — ¥24 billion of revenue, positive free cash flow — is being ascribed an enterprise value of only a few hundred million renminbi.

Source: cash and short-term investments (¥3.98bn, US$568.7m) per FY2025 Annual Report [28]; market value derived from ~354m ordinary shares [29] and a recent ADS price near US$2.58 (April 2026), consensus data feed.

This is the setup a value or special-situation investor is drawn to, and it is worth stating both what it offers and what it does not. It offers genuine downside support: a company generating cash and holding more cash than its market value is hard to zero out, which speaks directly to bankruptcy risk. It does not, by itself, offer a return. The cash has been static-to-declining — the pile fell from ¥5.31 billion in 2023 to ¥3.98 billion in 2025 as the company repaid borrowings [30] — the company pays no dividend, and a controlled company can hold cash indefinitely without returning it. The comparison is also sensitive to the share price, which has been volatile; the two analysts covering the stock carry a mean target near US$3.35, at which the market value would exceed the cash.

Who controls it, and who backed it

Dingdong is a founder-controlled company. Changlin Liang, the founder, chairman, and CEO, beneficially owned about 25.2% of the share capital but 80.9% of the voting power at the end of 2025, through Class B shares that carry 20 votes each against one vote for the Class A shares that trade as ADSs [31]. The company is a "controlled company" under NYSE rules and is exempt from the requirement that a majority of its board be independent [32]. For an investor who prizes founder skin in the game, the alignment is real; the same structure also means minority holders have little formal say and cannot force a sale or a payout.

The register of prior backers is the other half of the story. The IPO — which raised only about US$95.7 million, three-quarters of it taken up by affiliates of existing shareholders [33] — priced this as a marquee growth name. Its cap table still lists General Atlantic (5.5%), a SoftBank Vision Fund vehicle (5.9%), and Sequoia China / HongShan (4.7%), alongside Liang's holding companies [34]. A stock once owned by those names, down roughly 90% from its IPO price and covered by two analysts, is exactly the kind of once-loved, now-ignored situation where mispricing can persist.

What forward estimates imply

The thin analyst coverage — two estimates — expects the profit trend to continue and steepen: consensus revenue of ¥27.0 billion for 2026 (up about 11%) and ¥29.0 billion for 2027, with earnings expected to roughly double off the 2025 base [35]. Those are the numbers a bull leans on and a skeptic should stress-test; the forward financials, insider economics, and industry backdrop each warrant their own fuller treatment later in this report.

The question this report addresses

Dingdong is a fallen grocery-delivery star with a rare shape: restored profitability, positive free cash flow, and a net-cash balance sheet worth close to its whole market value, wrapped inside a founder-controlled Chinese ADR in a fiercely competitive market. The question the following chapters work through is whether that restored profitability is durable enough — and the balance sheet protective enough — to make a stock trading near its own cash a genuine margin-of-safety opportunity, or whether thin margins, decelerating growth, China's instant-retail price war, and the governance and delisting overhang leave it a value trap in which the cash is real but the return never arrives.

The Financial Record

Three audited years show a genuine but fragile turnaround. Revenue recovered from a 2023 retrenchment to a record RMB24,359.9 million in 2025, and Dingdong reached GAAP profit for the first time [1]. But the net margin is about 1%, gross margin is drifting down, and almost all of the reported profit comes from government subsidies and interest on the cash pile rather than from selling groceries [2]. Consensus rests on two analysts — and a pending sale to Meituan changes what these numbers mean.

The revenue arc: retrenchment, then a decelerating recovery

Dingdong's top line is not a smooth growth story. After the 2021 strategic pivot to "efficiency first with due consideration of scale," the company exited cities and cut back, and revenue fell 17.5% in 2023 to RMB19,971.2 million. It then recovered to RMB23,066.3 million in 2024 (+15.5%) and edged to a record RMB24,359.9 million in 2025, but growth had decelerated to 5.6% [3].

Source: FY2025 Annual Report (Form 20-F), Operating Results — 2023–2025 figures [4]; 2022 from the FY2024 Annual Report income statement [5].

The recovery is real but shallow, and the mix underneath it is softening. Average order value slipped from RMB72.1 in 2023 to RMB71.4 in 2024 and RMB70.1 in 2025, which management attributes to "declining consumer prices for certain commodities" [6]. In other words, order counts are carrying growth while price per basket falls — the footprint of deflation and competition in China's grocery market, not pricing power.

Where the profit actually comes from

The three-year record establishes where the profit actually comes from. In 2025, total revenues of RMB24,359.9 million minus total operating costs and expenses of RMB24,373.2 million left the core grocery operation at a loss of roughly RMB13 million — before any other income [7]. The reported RMB131.7 million of operating income exists because of "other operating income, net" of RMB145.0 million — which the company says rose mainly on RMB26.4 million more in government subsidies [8]. Government subsidies alone were RMB87.4 million in 2025, up from RMB61.0 million in 2024 and RMB18.1 million in 2023 [9].

Below the operating line, RMB125.6 million of interest income — earned on the cash and short-term investments — net of RMB16.8 million interest expense, lifted pre-tax income to RMB240.9 million [10]. Split the profit into its three drivers across the three years and the pattern is clear: the grocery operation hovers around breakeven, while subsidies and interest on the balance sheet do the work.

Source: derived from the FY2025 income statement — core operations = total revenues less total operating costs; other operating income, net; interest income less interest expense [11].